In the rapidly evolving world of instant payments, the introduction of the FedNow Service in July 2023 marked a significant milestone. This guide has been created to provide banks and credit unions with a better understanding of the FedNow Service, as well as the resources needed to find out more information. Alacriti facilitates a connection between financial institutions and the FedNow Service (as well as other rails) through its Orbipay Payments Hub solution. The below frequently asked questions about the FedNow Service should address many of the common misconceptions and questions that financial institutions may have.

Source: © 2023 Federal Reserve Banks, © 2023 Federal Reserve

Navigating the process is now more seamless than ever. Here is an overview of how it works.

The FedNow Service makes it possible to initiate payments seamlessly by transmitting payments messages through the end-user interface to financial institutions. The financial institution will then receive instructions to authorize the transaction, subsequently sending a payment message to the FedNow® Service. At this time, the FedNow Service will validate any payment messages and send them to the financial institution for either acceptance or rejection. Upon completion, the financial institution will send a response to the FedNow Service confirming the final decision.

In the event of rejection, the FedNow Service informs the payee. If accepted, the FedNow Service deducts funds from the payor’s account and credits them to the payee’s account.

Here’s a breakdown of this 10-step process that occurs within seconds:

Source: © 2023 Federal Reserve Banks, © 2023 Federal Reserve

Navigating the process is now more seamless than ever. Here is an overview of how it works.

The FedNow Service makes it possible to initiate payments seamlessly by transmitting payments messages through the end-user interface to financial institutions. The financial institution will then receive instructions to authorize the transaction, subsequently sending a payment message to the FedNow® Service. At this time, the FedNow Service will validate any payment messages and send them to the financial institution for either acceptance or rejection. Upon completion, the financial institution will send a response to the FedNow Service confirming the final decision.

In the event of rejection, the FedNow Service informs the payee. If accepted, the FedNow Service deducts funds from the payor’s account and credits them to the payee’s account.

Here’s a breakdown of this 10-step process that occurs within seconds:

Source: https://fasterpaymentscouncil.org/use-cases

A2A: Investments →Apple Cash allows for instant credit, which can subsequently be used for other wallet transactions.

B2B, B2G, G2B, G2G: UPS/FedEx → Immediate payment in full upon delivery acceptance (cash on delivery).

B2C: Transportation/Delivery/Personal Service → Delivery service where payment gets sent in addition to tips in real time.

C2B, C2G: Food & Beverage → Restaurants need contactless payment and aim to avoid the cost of interchange and chargebacks. They have sensitive cash and can gain an advantage from immediate access.

G2C: Government Services → Some examples include social security, welfare, disability, and unemployment.

P2P: Non-Industry Specific Use Cases → Child support and situations where several people split the cost of rent or another purchase are a couple of instances (connected to the same reference information).

Source: https://fasterpaymentscouncil.org/use-cases

A2A: Investments →Apple Cash allows for instant credit, which can subsequently be used for other wallet transactions.

B2B, B2G, G2B, G2G: UPS/FedEx → Immediate payment in full upon delivery acceptance (cash on delivery).

B2C: Transportation/Delivery/Personal Service → Delivery service where payment gets sent in addition to tips in real time.

C2B, C2G: Food & Beverage → Restaurants need contactless payment and aim to avoid the cost of interchange and chargebacks. They have sensitive cash and can gain an advantage from immediate access.

G2C: Government Services → Some examples include social security, welfare, disability, and unemployment.

P2P: Non-Industry Specific Use Cases → Child support and situations where several people split the cost of rent or another purchase are a couple of instances (connected to the same reference information).

What is FedNow?

The FedNow® Service represents the Federal Reserve’s entry into modernizing payments with a service that enables instant, 24/7 money transfers for financial institutions. It is the newest payment rail in the United States. The FedNow Service aims to give businesses and people an effective way to pay and instantaneously access funds through their financial institutions. The financial institutions and their consumers benefit from a real-time payment option.How does FedNow work?

Source: © 2023 Federal Reserve Banks, © 2023 Federal Reserve

Navigating the process is now more seamless than ever. Here is an overview of how it works.

The FedNow Service makes it possible to initiate payments seamlessly by transmitting payments messages through the end-user interface to financial institutions. The financial institution will then receive instructions to authorize the transaction, subsequently sending a payment message to the FedNow® Service. At this time, the FedNow Service will validate any payment messages and send them to the financial institution for either acceptance or rejection. Upon completion, the financial institution will send a response to the FedNow Service confirming the final decision.

In the event of rejection, the FedNow Service informs the payee. If accepted, the FedNow Service deducts funds from the payor’s account and credits them to the payee’s account.

Here’s a breakdown of this 10-step process that occurs within seconds:

- Step 1: This transaction will occur between the payee and the payee’s financial institution.

- Step 2: The payor initiates a payment by sending payment messages to the bank or credit union.

- Step 3: The bank or credit union will then receive instructions and proceed to authorize the transaction if sufficient funds are available.

- Step 4: The bank or credit union contacts and submits the payment message to the FedNow Service.

- Step 5: The service will validate the payment message and subsequently send it back to the bank or credit union, indicating either acceptance or rejection.

- Step 6: In the event of rejection by the bank or credit union, no further action will occur. However, upon acceptance, Fednow promptly deducts those funds and credits them to the payee’s account.

- Step 7: The service will either debit or credit the sender and receiver financial institutions’s authorized account. Steps up to this point will take up to 20 seconds to complete.

- Step 8: To notify both parties of the payment, the service will send an advisory to the receiver financial institution and an acknowledgment to the sender financial institution.

- Step 9: The receiver financial institution can choose to confirm the posting by sending a message to the sender financial institution.

- Step 10: Finally the Fednow Service notifies everyone of the successful transaction. In instances where the financial institution rejected the transaction in step 6, the FedNow Service notifies all parties of the rejection.

How can FedNow help banks and credit unions?

For Credit Unions: When choosing between credit unions and banks, the younger generation often leans towards banks due to perceived modernity. Zoomers form a relatively small portion of credit union (CU) members, which raises the question of why. This might be attributed to banks’ technological advancements and robust campus marketing. However, with connection to the FedNow Service available to all financial institutions, credit unions can now more closely align with the immediate gratification that Zoomers expect. For Banks: The FedNow Service presents another opportunity for banks to improve their customer experience. As banks actively promote their instant payment services, the addition of the FedNow Service broadens their reach for financial institutions that participate in instant payments. For All Financial Institutions: The FedNow Service will enhance liquidity management by introducing streamlined transfer capabilities, promoting efficiency for credit unions and banks. This directly benefits financial institutions and their accountholders, as the expedited process contributes to increased customer satisfaction. In addition, banks and credit unions that are struggling with processing and exceptions (associated with wires and ACH), may find relief in the fully automated FedNow Service. The result is better back-office efficiency.How can the FedNow Service help bank customers and credit union members?

Improve Efficiency: The FedNow Service can improve efficiency for bank customers and credit union members. Customers and members demand speed and efficiency, especially in times of emergency. Customers can access funds immediately using the FedNow Service, resulting in faster access to funds. This is helpful for any accountholder, but is especially valuable for those who are not able to wait for conventional settlement timeframes. Lowering Cost and Improving Management: Forward-thinking financial institutions equip their customers and members with personal finance tools to help manage their money. Offering instant payments helps accountholders better predict and manage their money, and avoid the frustration of unnecessary NSF fees. Not to mention for business owners, there can be faster settlements which can lead to minimizing administrative costs and enhancing the overall financial management. Technological Advances: The addition of the FedNow Service will assist businesses in developing better and more pleasant ways to improve customer experience. Overall, the FedNow Service provides numerous opportunities for customers to have a better experience with their financial institutions. As technology is on the rise, providing customers with more convenient solutions than ever, so are the demands on banks and credit unions to enhance their customer experience with products that address their needs. For instance, a car loan disbursement over the weekend so a customer can drive out of the dealership with a new car on a Saturday.What are the use cases for FedNow?

Source: https://fasterpaymentscouncil.org/use-cases

A2A: Investments →Apple Cash allows for instant credit, which can subsequently be used for other wallet transactions.

B2B, B2G, G2B, G2G: UPS/FedEx → Immediate payment in full upon delivery acceptance (cash on delivery).

B2C: Transportation/Delivery/Personal Service → Delivery service where payment gets sent in addition to tips in real time.

C2B, C2G: Food & Beverage → Restaurants need contactless payment and aim to avoid the cost of interchange and chargebacks. They have sensitive cash and can gain an advantage from immediate access.

G2C: Government Services → Some examples include social security, welfare, disability, and unemployment.

P2P: Non-Industry Specific Use Cases → Child support and situations where several people split the cost of rent or another purchase are a couple of instances (connected to the same reference information).

Which banks or credit unions are using the FedNow Service today?

According to the Federal Reserve, over 1,500 financial institutions are now either receiving or both sending and receiving on the FedNow Service network as of November 2025. Adoption is already at a good start with most major banks using the FedNow Service. Its impact on efficiency and speed is especially significant when it comes to services related to payroll—receiving a paycheck immediately can be a game-changer for many. For instance, gig workers with variable hours, e.g., DoorDash drivers can now receive their earnings the same day they worked. The FedNow Services extends its services to more than 1,500 banks and credit unions, either directly or as intermediaries. The sole criteria for eligibility to use the FedNow Service is to be either a bank or credit union. Check here to see a list of financial institutions that are a part of this network.

What services compete with FedNow?

The RTP® network stands out as the primary direct competitor of the FedNow Service. The RTP network belongs to The Clearing House, which provides real-time payments that are all federally insured and eligible for swift and secure transactions from senders to receivers. In addition to core banking providers, the RTP network has established partnerships with major technology companies and funding agents. This platform consistently introduces innovative features to mitigate risk and increase consumer confidence, such as DDA Tokenization and Document Exchange.

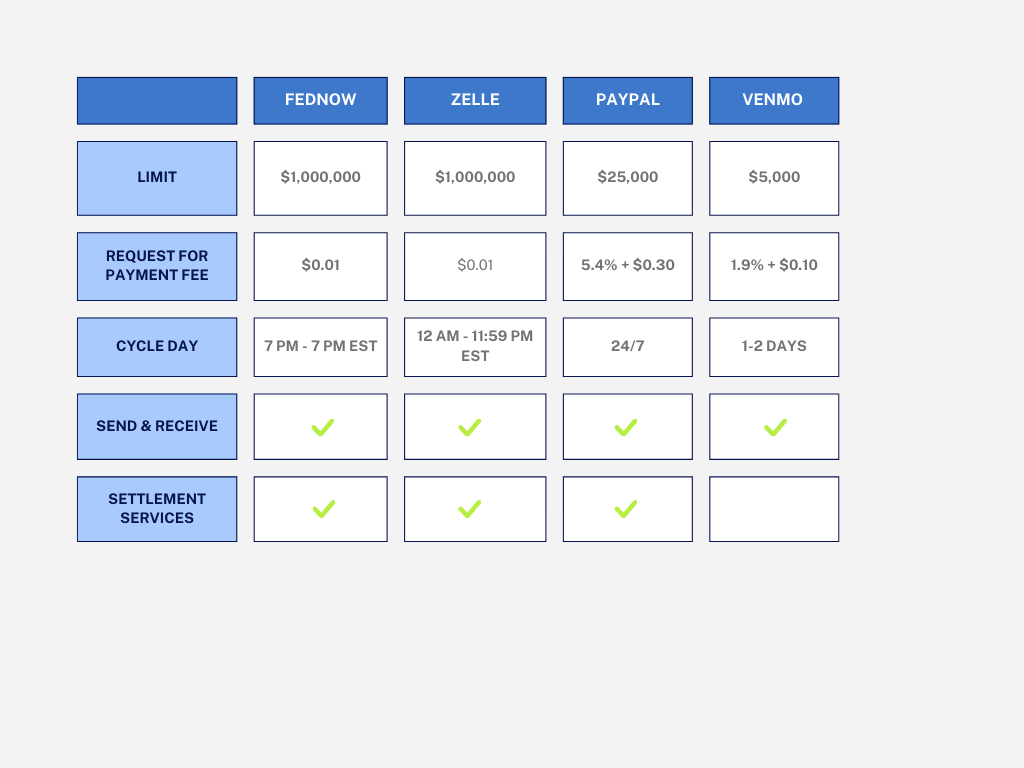

In addition to the RTP network, alternative services such as PayPal, Venmo, Zelle®, and MasterCard Send offer faster payment solutions. These platforms have established relationships with various companies, ensuring customers have an efficient payment process so they can receive or send their money easily.

What’s the difference between The Clearing House’s RTP Network and the FedNow Service?

Initiated in November 2017, the RTP network is overseen by The Clearing House, operates as a privately held system, and is owned by the largest commercial banks, such as Bank of America, TD Bank, BNY Mellon, and many more. More than 655 participants currently use the RTP network to send and receive real-time payments. Users can both initiate and request payments through the platform. The RTP network has processed over 1 billion transactions in a single day, on September 1, 2023, demonstrating consistent growth since its initial launch. The RTP network has recently introduced several innovative features. Among these features is IXB (Immediate Cross-Border Payments), as well as a Zelle partnership (a P2P service), which also has established partnerships with numerous banks and financial institutions. The original individual value limit was $25,000 as a risk-managed approach when TCH was first introducing the RTP network. After a successful rollout, there is now a limit of $10,000,000 per transaction.

Launched in July 2023, the FedNow Service is under the management of the Federal Reserve, a centrally owned system established in 1913. Some of the notable financial institutions that take part in the FedNow Service are JPMorgan Chase, Veridian Credit Union, and many more. As of September 2025, more than 1,500 financial institutions use the FedNow Service. Similar to the RTP network, this instant payments service operates continuously, providing services every day of the year, without limitations on weekends or holidays. While the platform ensures availability for sending and receiving payments at all times, it currently imposes a maximum volume limit of $10,000,000 for transactions as stated above. The FedNow Service, starting November 2025, will raise the limit to $10,000,000. However, the Federal Reserve regularly assesses and adjusts credit transfer limits as deemed necessary. The FedNow Service offers a range of options, including Send and Receive, Receive Only, liquidity management transfers, and settlement services.

The FedNow Service cycle day operates from 7 a.m. to 7 p.m. ET, while the RTP network cycle spans from 12 a.m. to 11:59 p.m. ET. The FedNow Service offers everything the RTP network does, as well as Liquidity Management Transfers (LMT), which are transfers between financial institutions in support of liquidity needs. The fee per transaction for senders is $0.045 for both services. However, the cost differs for sending a Request for Payment (RfP)–it’s $ 0.01 for the FedNow Service and $0.11 for the RTP network.

How much does the FedNow Service charge per transaction?

The enrollment fee for participation is $25 to receive credit transfers, with a fee of $0.045 per transaction, covered by the sender. Additionally, a $0.01 fee applies per request for payment (RFP) message, paid by the requester.What is the FedNow Service’s transaction limit?

While the transaction limit is set to increase to $10,000,000, it’s imperative to note that the Federal Reserve regularly reviews credit limits, making adjustments as deemed necessary.What’s the difference between the FedNow Service and Fedwire?

Fedwire functions similarly to FedNow, facilitating instant posting and settlement of payments. Nevertheless, distinctions exist between the two systems. The FedNow service operates seamlessly throughout the day, including holiday weekends and regular weekends, with more than 1,500 participants. In contrast, Fedwire does not operate on weekends and is subject to holiday restrictions, with more than 5,000 participants. In terms of transaction limits, the FedNow service, starting in November 2025, will impose a cap of $10,000,000. In contrast, Fedwire transactions do not carry a predefined limit; rather, the transaction limit for Fedwire is contingent upon the policies of the specific financial institution involved in the transaction.

Another way these two differ is in their hours of operation. Fedwire operates from 9:00 p.m. to the preceding day till 7:00 p.m. Monday through Friday. The FedNow Service is 7 p.m. to 7 p.m. 24 hours per day on weekends and Federal Reserve holidays. Fedwire does not operate 24 hours a day, unlike the FedNow Service, but may offer extensions by the Federal Reserve Banks.

What’s the difference between the FedNow Service and PayPal/Zelle/Venmo?

PayPal operates as a private money transfer service, distinguishing itself from the FedNow Service. In contrast to platforms such as PayPal, Zelle, and Venmo, users of the FedNow Service are required to go through their financial institution for access. PayPal, Zelle, and Venmo users can manage their account, send, request-to-receive, and receive money directly from the app. The FedNow Service offers swift money transfers by allowing users to send and receive money within seconds. Services such as Venmo impose a fixed rate of 1.75% on instant transfers sent to a credit union or bank account. For example, if someone is transferring $200 to their bank account, they incur a $3.50 fee, while a $50 transfer results in a $0.87 fee. Users may opt for a free transfer option, however, they are required to wait 1-3 business days. Depending on the financial institution, the FedNow Service requires a monthly fee of $25 and senders incur a $0.045 per credit transfer fee (including returns). Alternatively, a $0.01 fee is charged for the RfP (Request for Payment) which must be paid by the requesters.How can I get started with the FedNow Service, and how long will it take?

To initiate the usage of the FedNow Service, it is possible to connect directly or through a third-party service provider. Unlike direct-use platforms like Venmo or Zelle, the FedNow Service primarily functions as a service accessed through financial institutions. Before connecting, banks and credit unions should assess their systems and processes to identify necessary changes or modifications. There are two ways to participate in the FedNow Service. The minimum participation type is to be a receiving financial institution, which means the financial institution can receive payments and post them to accounts instantly. Financial institutions may have the perspective that their existing systems work well enough with ACH, checks, wires, credit, and debit cards. However, at a minimum, it’s essential to give accountholders the minimum capability to get their money into their account(s) as quickly as possible. This can be done through service providers like Alacriti (which would take around a few months), to have the Receive connectivity to bring the money into customer accounts, post, and make the funds available immediately. The next level in real-time payments is the capability to send. A receiving institution that elects to send has a little more work to do that goes into having that capability. They’re opening up for customers to move money out of their accounts. At that point, it’s necessary to make sure all of the security protocols and fraud mitigation tools are in place and have a way to ensure that members are not sending out money erroneously or getting defrauded. Also, with Send, that doesn’t mean that it’s necessary to open the capability up to everybody—there can be different Send capabilities and different limits for individual customers or business clients.When banks and credit unions are finally connected to FedNow, how fast do they typically receive transactions?

The speed of transactions is contingent upon several factors, including the technological infrastructure used by banks or credit unions and the efficiency of the technology itself. However, transactions can be received and or sent within a couple of seconds. The minimum time required for a transaction is a few seconds, while the maximum duration is up to a few minutes, depending on various considerations.Is it mandatory to open a separate account with the Fed for FedNow?

A financial institution can settle in its master account at the Federal Reserve if they have one, or it can settle with its correspondent bank. This can be done in the same way as other financial services products today. So a financial institution can settle the same way as it does its ACH, wires, and checks.

There’s no need to get any new accounts pre-funded. It can all flow through a correspondent account or directly into a financial institution’s master account.