Zelle® vs. Wire Transfer

Electronic payments have become an essential part of everyday life, but not all payment methods serve the same purpose. While Zelle® and wire transfers both facilitate payments between accounts, they differ significantly in terms of speed, cost, transaction limits, settlement, and ideal use cases. Understanding these differences can help consumers and businesses choose the right payment method for each situation.

What is Zelle®

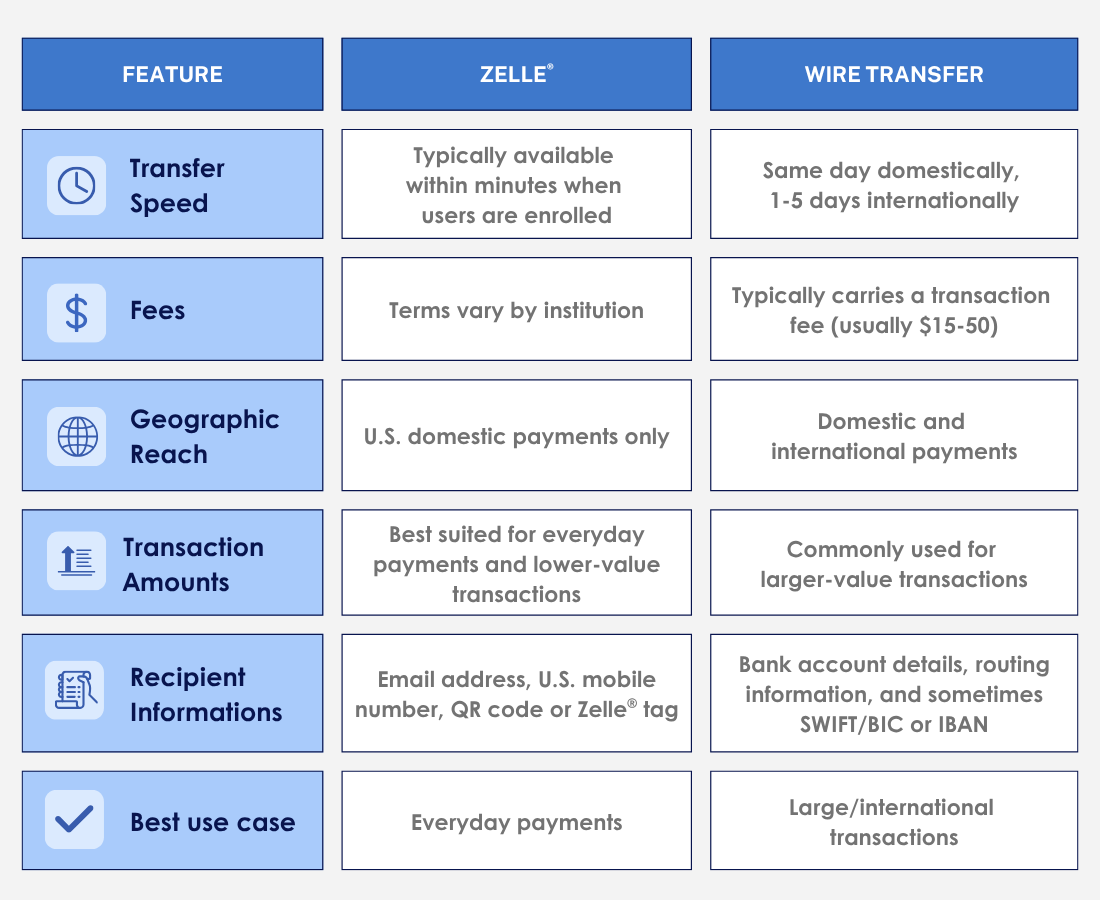

Integrated directly into banking apps, Zelle® facilitates bank-to-bank payments to enrolled users within minutes, without requiring a separate wallet balance. Operated by Early Warning Services, LLC, it allows users to send money using only a recipient’s email or U.S. mobile number.

However, Zelle® is not a wire transfer. Instead, it leverages the ACH network and existing banking infrastructure to enable faster P2P payments than traditional ACH processing.

Because of its speed and convenience, Zelle® is commonly used for:

- Splitting the cost of bills with friends or family

Zelle® is designed primarily for domestic U.S. transactions and does not support international payments. Transfer limits also vary depending on the participating bank or credit union. For consumers looking for a quick and convenient way to move smaller amounts of money domestically, Zelle® provides a fast and user-friendly experience.

What Is a Wire Transfer?

Wire transfers are direct electronic transfers between financial institutions, processed individually via dedicated networks like Fedwire (domestic) or SWIFT (international). Unlike ACH-based systems, wires provide Real-Time Gross Settlement (RTGS), making them the standard for high-value, time-sensitive transactions.

While domestic wires often settle the same day, international transfers can take 1-5 business days due to currency conversion and intermediary bank requirements. Although highly secure, wire transfers are generally irrevocable once processed.

- Primary Use Cases: High-value business transactions, real estate closings, and international vendor payments.

- Infrastructure: Operates via the Federal Reserve Wire Network (domestic) or SWIFT (international).

- Settlement: Offers immediate finality; once the transfer is sent, it is typically impossible to reverse.

- Required Data: Often requires specific identifiers such as IBAN numbers or SWIFT/BIC codes for cross-border accuracy.

Zelle® vs Wire Transfers: Key Differences

Although both Zelle® and wire transfers allow users to send money electronically, the two payment methods are not the same.

Choosing the Right Payment Method

The decision-making process typically hinges on whether the priority is speed-to-notification (Zelle®) or finality-of-settlement (Wire).

- Zelle® (P2P/Small Business): Best for quick, low-value domestic payments between trusted parties. It excels in the “convenience economy” where the average transaction size is small, and the recipient is a known individual or a registered small business.

- Wire Transfers (High-Value/B2B): The preferred method for high-value transactions that require Real-Time Gross Settlement (RTGS). Because wires are irrevocable, they are the requisite rail for real estate closings, large asset purchases, and legal settlements.

- The International Factor: Zelle® is strictly domestic. For any cross-border remittance or global supply chain payment, a wire transfer via the SWIFT network—or an International ACH (IAT)—is required.

Best Practices for Sending Payments

While both Zelle® and wire transfers are safe when used properly, users should always verify payment requests and recipient information before sending funds. Many payment scams rely on social engineering techniques, which use deception, impersonation, or a sense of urgency to persuade individuals to authorize payments or share sensitive information.

One common example is Business Email Compromise (BEC), where criminals impersonate executives, vendors, real estate agents, or business partners and request changes to payment instructions. These schemes often rely on spoofed or compromised email accounts to make requests appear legitimate.

Since Zelle® payments are sent quickly, users should only send money to trusted recipients. Similarly, wire transfers are often irreversible once completed, making it critical to verify payment instructions carefully before sending funds.

Here are some best practices:

- Verify recipient information carefully

- Use multi-factor authentication when available

- Confirm payment changes verbally

- Avoid sending money to unknown parties

- Monitor accounts regularly for suspicious activity

The future of payments is not about choosing a single rail—it’s about having access to the right rail for the right transaction. Whether the need is a real-time payment to a friend, a payment to a small business, or a high-value wire transfer, financial institutions are increasingly focused on providing seamless access to multiple payment options. The ability to support a variety of payment methods through a unified experience will continue to play an important role in meeting evolving customer expectations.

Alacriti’s centralized payment platform, Orbipay Payments Hub, provides innovation opportunities and the ability to make smart routing decisions at the financial institution to meet their individual needs. Financial institutions can take full ownership of their payments and control their evolution with TCH’s RTP® network, the FedNow® Service, Zelle®, Fedwire, ACH, and Visa Direct, all on one cloud-based platform. To speak with an Alacriti payments expert, please contact us at info@alacriti.com.

Zelle® and the Zelle® related marks are wholly owned by Early Warning Services, LLC and are used herein under license.