Solving Payment Fragmentation for Banks and Credit Unions

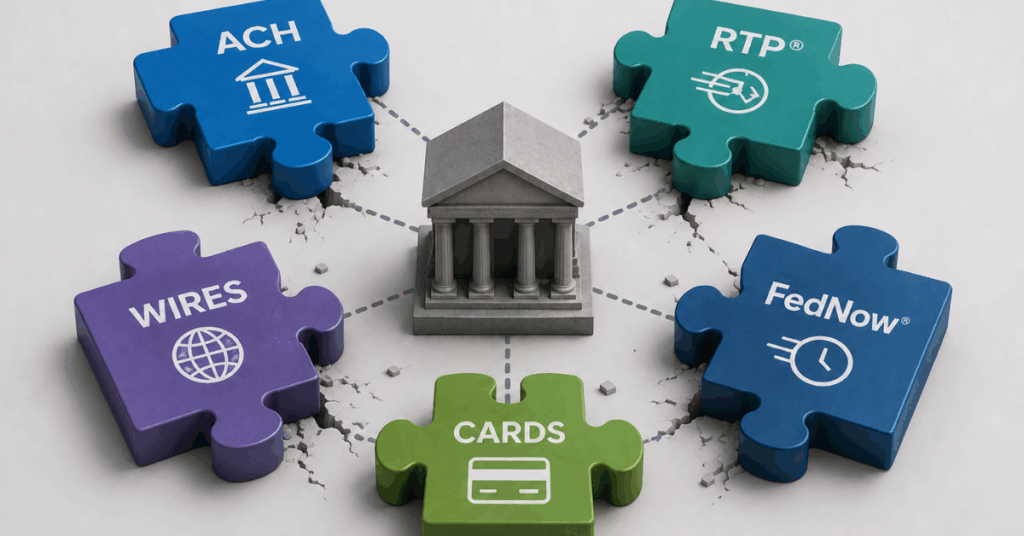

As time goes on, many banks and credit unions are finding themselves managing an increasingly fragmented infrastructure. ACH payments run through one system, wire transfers through another, and newer rails such as the RTP® network and FedNow® Service often require additional standalone platforms.

While supporting multiple payment types is essential, managing them through disconnected systems creates operational complexity, higher costs, and inconsistent user experiences. Over time, this fragmentation becomes more than just a technology challenge—it becomes a strategic one.

What Is Payment Fragmentation?

Payment fragmentation occurs when payment channels operate across multiple disconnected systems rather than through a single, unified infrastructure. For many financial institutions, this means managing separate vendors, workflows, compliance processes, and reconciliation methods for each payment rail.

Common issues include:

- ACH, wires, RTP, and FedNow operating on separate platforms

- Different cut-off times and approval workflows depending on the payment type

- Manual reconciliation across disconnected systems

- Separate fraud and compliance monitoring for each rail

- New payment capabilities being added as standalone integrations instead of part of a centralized strategy

The challenge isn’t necessarily a lack of payment capabilities—it’s the lack of cohesion between them.

The Cost of Payment Fragmentation

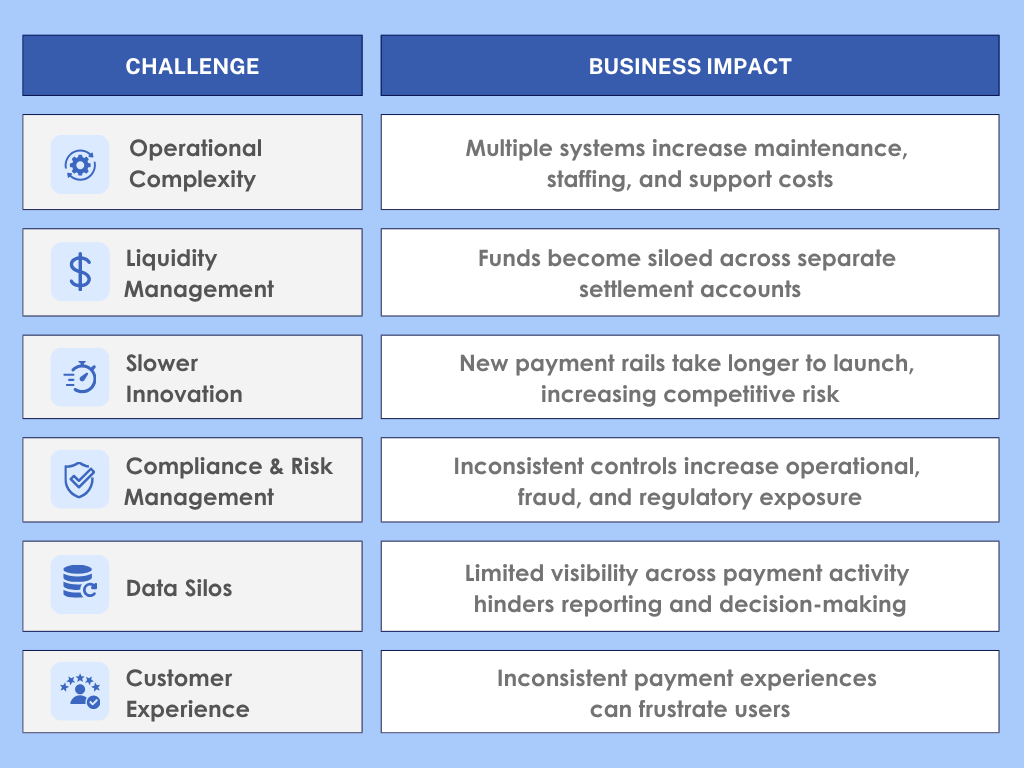

The impact of payment fragmentation extends far beyond technology. Supporting multiple payment systems often requires separate vendors, workflows, settlement processes, compliance controls, and operational teams. As institutions add new payment rails, costs rise alongside complexity, making payment operations more difficult to manage and scale.

Fragmented environments can also slow innovation. Instead of extending capabilities through a centralized infrastructure, financial institutions must repeatedly integrate, test, and support additional standalone systems. This can increase implementation timelines and make it more challenging to introduce new payment services.

At the same time, managing fraud detection, sanctions screening, AML monitoring, reconciliation, and reporting across disconnected systems can create operational inefficiencies and reduce visibility. Maintaining consistent controls and workflows becomes increasingly difficult as payment ecosystems grow.

The effects are often felt by customers and members as well. Different processing times, approval workflows, and payment experiences across channels can create friction and make it harder to deliver the seamless, consistent experiences that consumers and businesses increasingly expect.

The Shift Toward Unified Payment Infrastructure

With the growth of emerging payments rails, simply adding more systems is becoming increasingly unsustainable. Financial institutions need a way to address payment fragmentation without introducing additional operational complexity. This is why many banks and credit unions are moving toward a payments hub model. Rather than managing separate platforms, a payments hub provides a centralized infrastructure that connects payment processing, risk management, reporting, and operations through a single platform.

A modern payments hub helps banks and credit unions:

- Consolidate ACH, wires, RTP, FedNow, and other payment types into a single platform

- Intelligently route payments based on speed, cost, value, or payment type

- Apply consistent fraud detection, compliance, and risk controls across all transactions

- Gain improved visibility into payment activity, reporting, and liquidity management

- Accelerate the rollout of new payment capabilities without adding operational silos

- Deliver a more seamless and consistent customer and member experience

Payment fragmentation was manageable when institutions supported only a handful of payment types. Today’s environment is different. With instant payments, digital wallets, cross-border capabilities, and emerging payment technologies continuing to expand, the ability to orchestrate payments through a unified infrastructure is becoming a strategic necessity. Institutions that address fragmentation today will be better positioned to innovate, compete, and meet evolving customer expectations tomorrow.

Alacriti’s centralized payment platform, Orbipay Payments Hub, provides innovation opportunities and the ability to make smart routing decisions at the financial institution to meet their individual needs. Financial institutions can take full ownership of their payments and control their evolution with TCH’s RTP® network, the FedNow® Service, Zelle®, Fedwire, ACH, and Visa Direct, all on one cloud-based platform. To speak with an Alacriti payments expert, please contact us at info@alacriti.com.