Credit union members increasingly expect financial interactions to mirror the seamless experiences they get from consumer brands—fast, intuitive, proactive, and mobile-first. But while credit unions have made major strides in digital bill pay, many still rely on passive systems that wait for the member to take action. As delinquencies trend upward nationwide and member expectations for personalization continue to rise, a ‘bill presentment only’ strategy leaves a growing gap between what members expect and what they receive.

In the CUInsight-hosted webinar, Retention Starts With a Reminder: The Impact of Digital Outreach, Stuart Bain, SVP of Product Management at Alacriti, explored why proactive outreach works, helpful tactics to drive results, and how credit unions can operationalize outreach without adding staff burden.

Quick Links

The Power of Proactive Digital Outreach

For many credit unions, the shift to digital payments solved the issue of convenience—but not the issue of engagement. Members can pay online, but they may still fall behind if communication is only available if they log in, or they have to remember due dates on their own. Proactive outreach bridges that gap by meeting the member where they already are—in their mobile inbox, text thread, or preferred channel—instead of requiring them to seek out a payment portal.

Unlike passive billing, proactive engagement interrupts the friction point before it becomes delinquency. A short reminder or prompt reduces the mental load on members and reinforces the idea that the credit union is helping simplify their financial life, not just notifying them of an obligation. This is increasingly where modern payment journeys are won or lost: not at the moment of payment, but in the moments leading up to it.

One of the biggest misconceptions is that outreach must be complex or require extensive marketing resources to build campaigns. In reality, the most effective strategies often stem from simple automation tied to timing and relevance. As Bain explained, “If you can prompt them at the right moment, you are helping them instead of chasing them later.” Proactive engagement reduces friction for the member and lightens the operational load for the institution—a dual benefit that traditional reminder strategies rarely deliver.

These reminders also shift the frame from ‘collections’ to ‘support.’ When members perceive outreach as assistance rather than pressure, adoption tends to follow organically. “It’s really about taking the work off the member,” Bain said. That reframing is central to why these programs often outperform portal-only journeys or static billing notices.

Audience Poll: How Credit Unions Are Currently Notifying Members

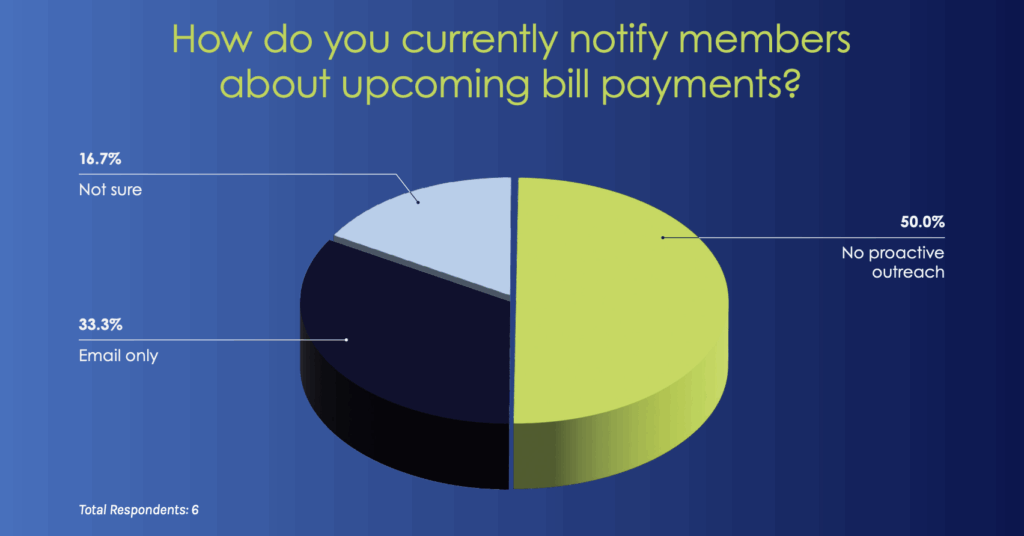

To gauge where credit unions stand in their member engagement efforts, the webinar opened with a poll asking how attendees currently notify members about upcoming payments: ‘How do you currently notify members about upcoming bill payments?’ Choices included Email only, Text message only, Both email and text, No proactive outreach, and Not sure. Results showed that 50.0% selected No proactive outreach, 33.3% chose Email only, and 16.7% responded Not sure. No respondents selected Text message only or Both email and text.

This gap between capability and action reflects one of the biggest challenges credit unions face today. Even as digital communication channels expand, many institutions are still waiting for members to initiate payments—effectively creating a ‘reactive’ experience in a world where members expect seamless, anticipatory service.

When reviewing the data, Bain observed how strategies differ by institution type:

Tactics That Work

Once institutions recognize the value of proactive engagement, the next question becomes: what types of outreach actually drive results? The most successful approaches have a few things in common—they are timely, relevant, and simple for the member to act on immediately. Rather than pushing members back into a portal or requiring multiple authentication steps, the most effective outreach strategies reduce friction and shorten the path from reminder to payment.

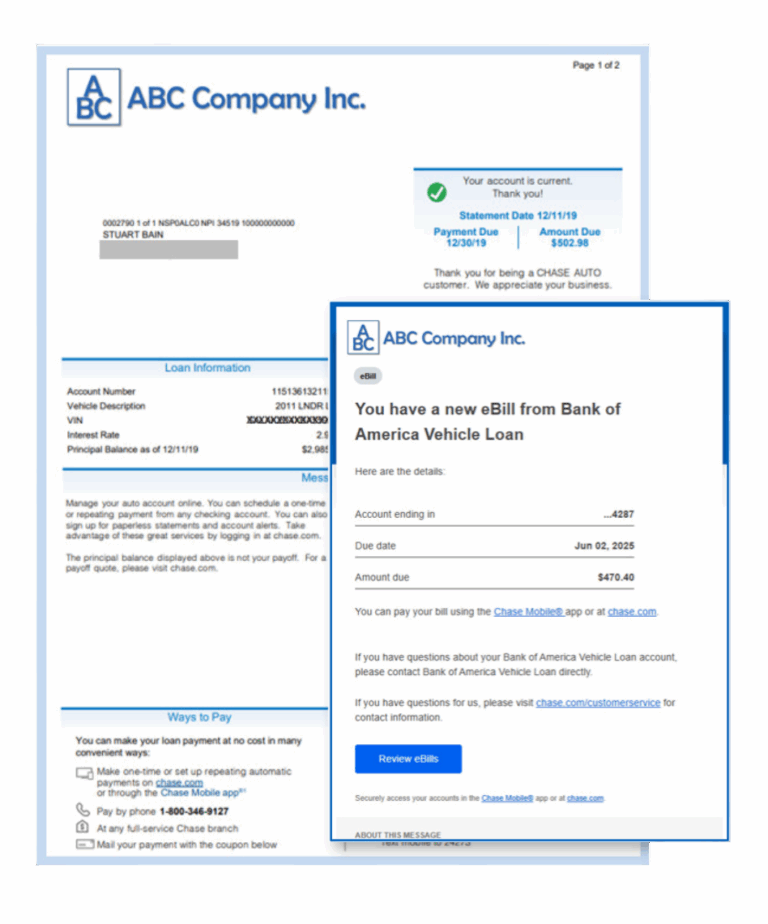

One of the strongest performing tactics discussed during the session is linking reminders directly to the payment action. When members don’t have to go searching for login credentials or navigate a multistep portal journey, payment completion rates rise. As Bain explained, “These can be used in place of, or in addition to, outbound calls,” demonstrating how digital reminders can shoulder a heavy operational lift while also improving the member experience.

Another tactic is adjusting outreach timing to intervene before delinquency rather than after it. A message sent several days before a missed payment is not only more effective—it also feels more supportive than corrective. The earlier the nudge, the less pressure the member feels, and the stronger the likelihood of payment.

The power of these tactics lies not in complexity, but in consistent execution. A well-timed reminder with a direct payment link outperforms post-delinquency notices every time, not because it is more aggressive, but because it prevents the friction point entirely. In this way, outreach becomes less about messaging and more about orchestration—removing barriers that prevent members from completing their intent to pay.

Ad-Hoc Outreach via CSR Bill Notifications

- Members or 3rd parties

- Send via email or text

- Select payment amount

- Set expiration date & time

- No standard or custom member messages

Audience Poll: When Outreach Is Actually Sent

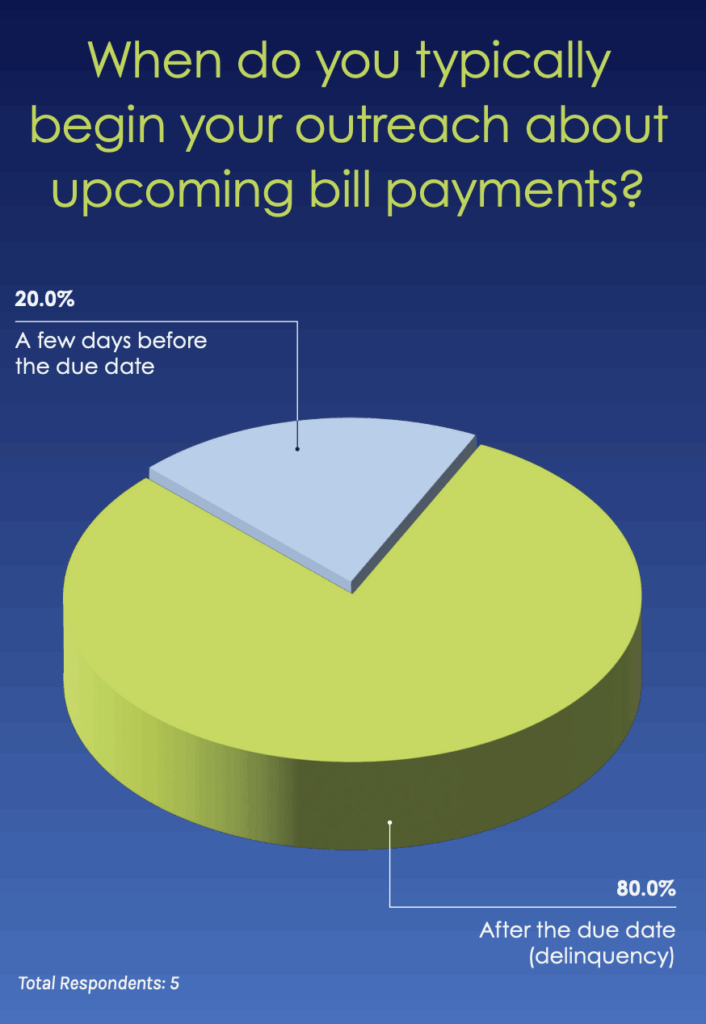

The second poll asked attendees when they typically begin outreach to members: ‘When do you typically begin your outreach about upcoming bill payments?’ Choices included: A few days before the due date, The day the bill posts, After the due date (delinquency), and Not sure. Results showed that 80.0% of respondents begin outreach after the due date (delinquency), while 20.0% indicated they start a few days before the due date. No attendees selected the day the bill posts, and none responded Not sure.

These results reveal an important pattern: even when institutions are communicating with members, most engagement begins too late to influence behavior upstream. By waiting until delinquency, credit unions shift from prevention to recovery—creating greater operational burden and a less supportive experience for members.

Bain reacted to the findings by noting, “The payment reminder, that was what I expected to see, only sending outreach after delinquency. That’s a very interesting and high score.” The data reinforces why timing is just as critical as channel: outreach is most effective when it precedes the problem, not follows it.

Driving Loyalty Through Better Experiences

For credit unions, proactive outreach is not just a payment strategy—it is a relationship-building strategy. When members feel supported rather than reminded, they experience the institution as a partner in their financial lives rather than a collector. This emotional shift is what turns routine transactions into moments of loyalty, especially for members who manage most of their financial obligations from a mobile device.

Digital outreach also removes guesswork for the member. Instead of searching through a portal or calling the branch for assistance, they receive exactly the information they need—at the moment they need it—in the channel they are already using. This reduces cognitive load and positions the credit union as anticipatory rather than reactive, which is a defining characteristic of modern digital-first service models.

It also improves internal confidence that outreach is doing more than nudging payment—it is reinforcing trust. When members consistently experience seamless reminders rather than disruptions or surprises, it deepens their preference for the institution. In an era where switching providers is increasingly easy, experience now plays as much of a role in retention as pricing or product.

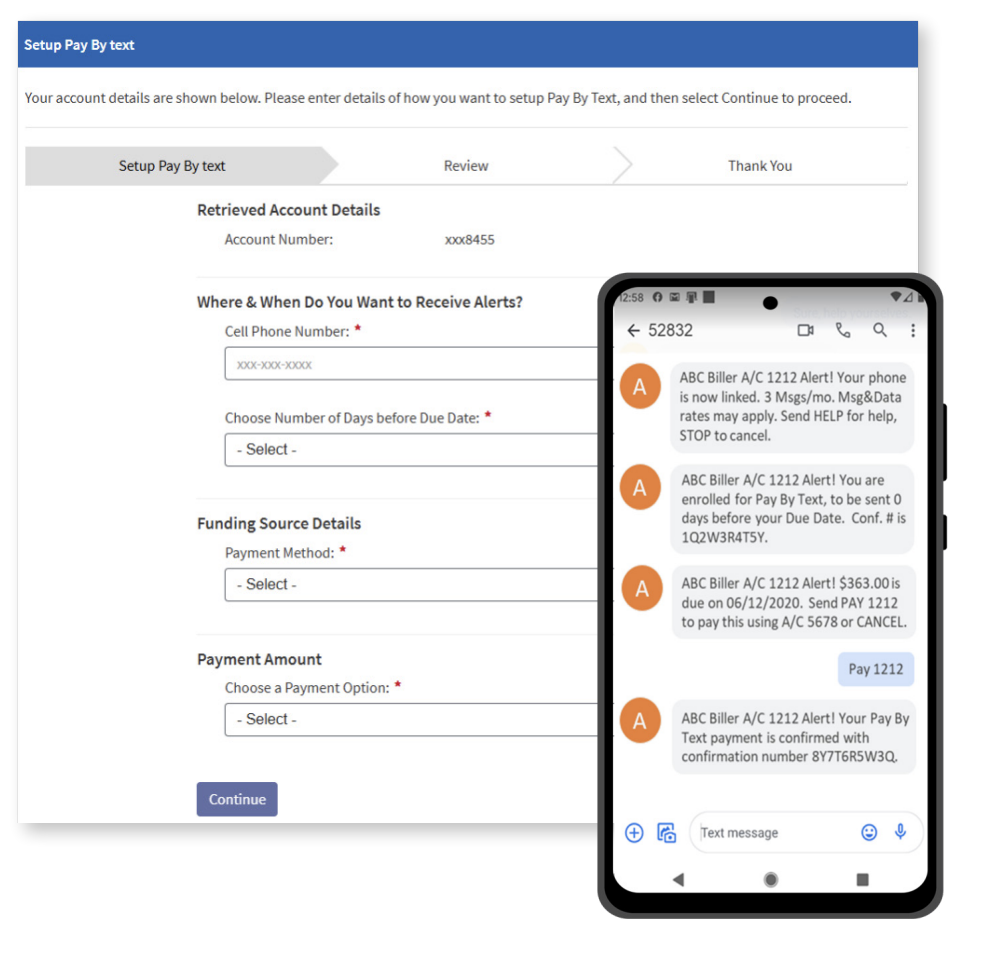

Pay by Text: Combining Outreach & Payments

How to Get Started

The key is to treat digital outreach as part of payments orchestration, not marketing. That means aligning reminders with member intent, not broad communications. Even a single automated reminder— delivered before delinquency—can begin shifting behavior toward routine digital adoption. “It doesn’t need to be complicated; it just needs to be consistent,” Bain said.

Another best practice discussed during the webinar was keeping the member’s path to action as short as possible. A reminder that forces the member to reauthenticate, navigate menus, or search for the payment screen introduces friction that reduces follow-through. The most effective implementations remove steps rather than add them— particularly for mobile-first members.

Institutions that are early in their journey often start with a single workflow—such as due-date reminders or pre-delinquency outreach— and gradually expand from there. This approach allows internal teams to quickly validate value without a large deployment effort. Over time, additional triggers can be layered in, reinforcing habits that keep payments current while improving operational efficiency.

An audience member asked about the risk of ‘over-messaging’ members. Bain stated that “Sending a reminder on the due date. ‘Hey, your bill’s due today.’” is a common approach. While this type of outreach is standard, the discussion clarified that volume is less important than timing—reminders should feel anticipatory rather than corrective. By prompting members before a potential issue arises, credit unions can turn outreach from a simple reminder into a meaningful service touchpoint that both supports members and reduces operational burden.

8 Things to Consider as You Prepare for Your Digital Outreach Journey:

Have you obtained consent for outreach?

Have you obtained consent for outreach?

Will you send emails and texts yourself or outsource it?

Does your chosen solution support the required notifications?

Does your payment service provider support magic links?

Can you support ad-hoc outreach initiated via CSRs?

Does your payment service provider support pay by text?

Why Proactive Outreach Matters Now

As member expectations continue to shift toward seamless, mobilefirst interactions, outreach is no longer just a courtesy—it is a core part of the payment experience. By reaching members before delinquency, and by simplifying the path from reminder to completion, credit unions can reduce friction, protect relationships, and increase digital adoption without adding operational burden.

The most successful strategies are not the most complex—they are the most timely. A well-placed reminder does more than trigger a payment; it reassures members that their credit union is anticipating their needs rather than reacting after a problem arises. In a competitive landscape where experience drives retention, proactive communication has become a differentiator in itself.

For institutions ready to take the next step, modern outreach platforms make it possible to automate these touchpoints, significantly shorten the payment journey, and scale engagement without staff intervention. With solutions like Orbipay Loan Payments, credit unions can integrate reminders, real-time payments, and mobile-friendly journeys into a single workflow—turning every nudge into an opportunity to deepen loyalty and streamline collections.

To dive deeper into how proactive digital outreach improves payment performance, reduces delinquency, and strengthens member loyalty, you can watch the full webinar, Retention Starts With a Reminder: The Impact of Digital Outreach.

Alacriti’s Orbipay Loan Payments is a customizable electronic billing and payments solution for businesses and financial institutions of all sizes. Orbipay Loan Payments offers convenient and flexible choices that include all the payment channels, payment methods, and payment options expected from a modern digital bill pay experience.