The growing challenge for many financial institutions is rethinking how bank account verification fits into today’s payments environment. Legacy validation methods were built for slower rails and delayed settlement. Still, they are increasingly strained as real-time payments become more common and customer tolerance for friction continues to shrink. Institutions are now asked to balance stronger ownership controls with seamless digital experiences—often at the exact moment a payment is initiated.

In the discussion Smarter Bank Account Verification, Better Risk Management, Stuart Bain, SVP of Product Management at Alacriti, examined how account verification is evolving in a real-time payments environment. The perspectives shared explored why ownership verification is becoming central to payments risk management. And how instant and same-day rails are reshaping the timing and mechanics of verification, while also addressing the growing need to balance fraud prevention with operational efficiency and user experience as faster payments become the norm.

Quick Links

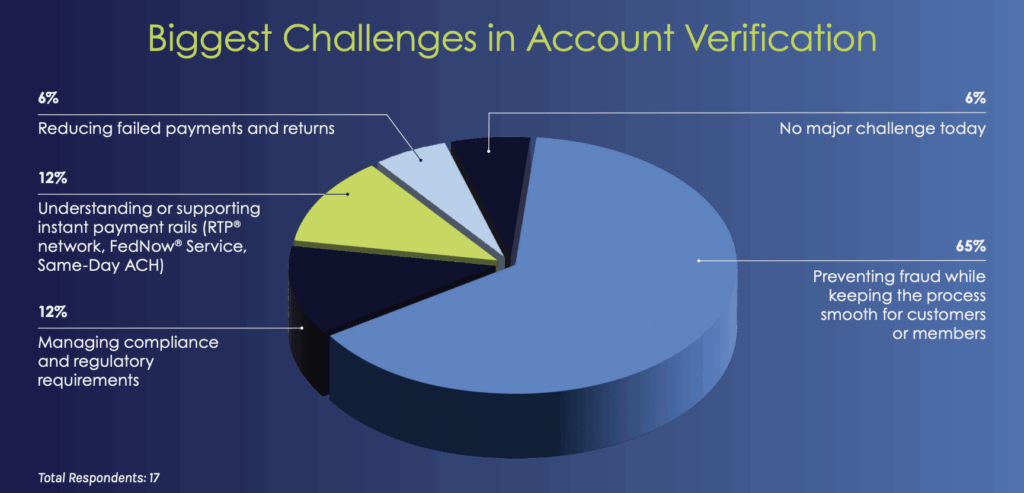

Audience Poll: Biggest Challenges in Account Verification

The webinar began with a poll. The audience was asked to identify their institution’s biggest challenge with account verification today. The responses revealed a clear concentration on balancing risk mitigation with customer experience.

The results highlight the tension institutions face between mitigating fraud risk and maintaining a smooth digital experience, with fraud-related concerns outweighing operational or compliance challenges.

Market Update

Payments are moving faster than the systems designed to support them. Across consumer and business use cases, immediacy has become the baseline expectation rather than a premium feature. Onetime payments, last-minute funding, and alert-driven actions now dominate activity, narrowing the window for financial institutions to verify accounts, assess risk, and complete transactions.

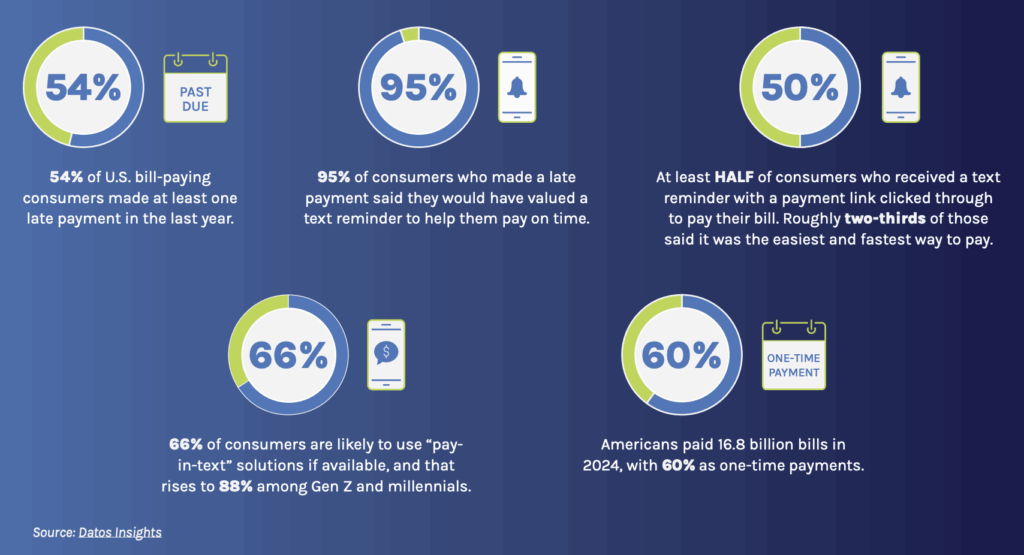

Recent data shared reflects this. Over 50% of U.S. consumers made at least one late payment in the past year, often driven by timing constraints rather than intent. At the same time, reminder-based payment experiences—particularly those delivered via text with embedded links—are driving faster completion rates. Together, these patterns reinforce a broader trend: payments are increasingly initiated at the moment of awareness, leaving little tolerance for delay. As Bain noted, “A lot of these payments are happening very close to the wire,” which fundamentally changes how verification and settlement must operate.

That behavioral shift is unfolding alongside rapid adoption of instant payments. Real-time payment volumes have climbed sharply, and participation across networks continues to expand. Bain pointed out that “70% of financial institutions now support real-time payments in credit transfers,” creating a meaningful inflection point for verification strategy. For institutions operating within that majority, verification can occur almost immediately. For the remaining segment, same-day ACH has emerged as a practical fallback to avoid multi-day delays.

Importantly, bill pay has emerged as one of the most influential drivers behind instant payment adoption. Institutions enabling realtime sending increasingly cite bill payments as a primary use case (now 52%), reflecting how closely payment urgency and verification requirements have become linked. When customers add a new account to pay a bill or fund an obligation, the expectation is no longer that verification will happen later—it is expected to happen immediately, or the transaction may be abandoned altogether.

From a risk perspective, this shift introduces new tradeoffs. Faster rails remove float and settlement uncertainty, but they also eliminate the buffer institutions historically relied on to identify errors or bad actors after the fact. As Bain explained, real-time rails force institutions to “make that decision up front,” shifting risk controls earlier in the payment lifecycle. Verification, therefore, becomes less about post-transaction cleanup and more about pre-transaction certainty.

Consumers Demand Real-Time, Frictionless Payment Experiences:

Ownership Verification

As payment speeds increase, the limitations of traditional bank account validation become more apparent. Validation confirms that an account and routing number are structurally correct. It does not confirm who controls the account. In a real-time environment, that distinction matters.

Ownership validation confirms that an account exists, while verification confirms that the user initiating a transaction actually owns it. Bain drew a clear line between the two concepts, explaining, “Validation is just the basic check that the account number is valid for the routing and transit number that’s been put in,” while verification is the step that confirms ownership and materially reduces risk.

This distinction became more consequential after the Nacha Web Debit Rule took effect in 2021, which mad4evalidation mandatory for new accounts used in web payments. While the rule established a crucial baseline, it left the method of validation open-ended—manual, batch, or real-time. That flexibility addressed compliance, but it did not address the growing need for certainty in faster payment flows. As Bain framed it, validation answers whether the account looks right; verification answers whether it belongs to the person using it.

Ownership verification also plays a direct role in reducing downstream issues such as ACH returns. By confirming account access before initiating a payment, institutions can eliminate many return scenarios tied to incorrect or unauthorized account use, ensuring the account is open, valid, and accessible at the time of transaction.

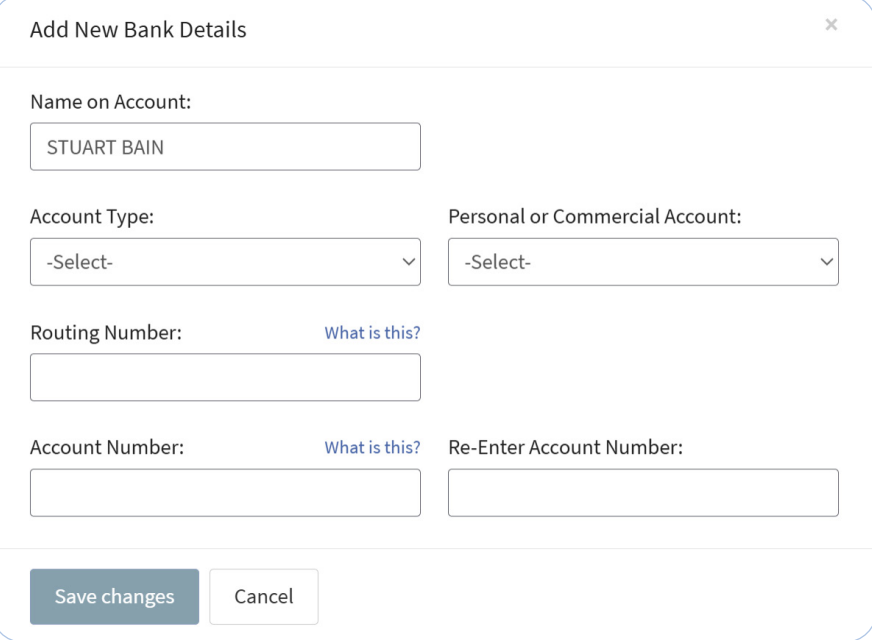

There are three primary approaches institutions use today:

Manual methods, such as requesting check images or bank statements, remain in use but introduce friction and delay

Challenge deposits, which improve on the manual experience, but have historically relied on ACH credits that can take days to settle

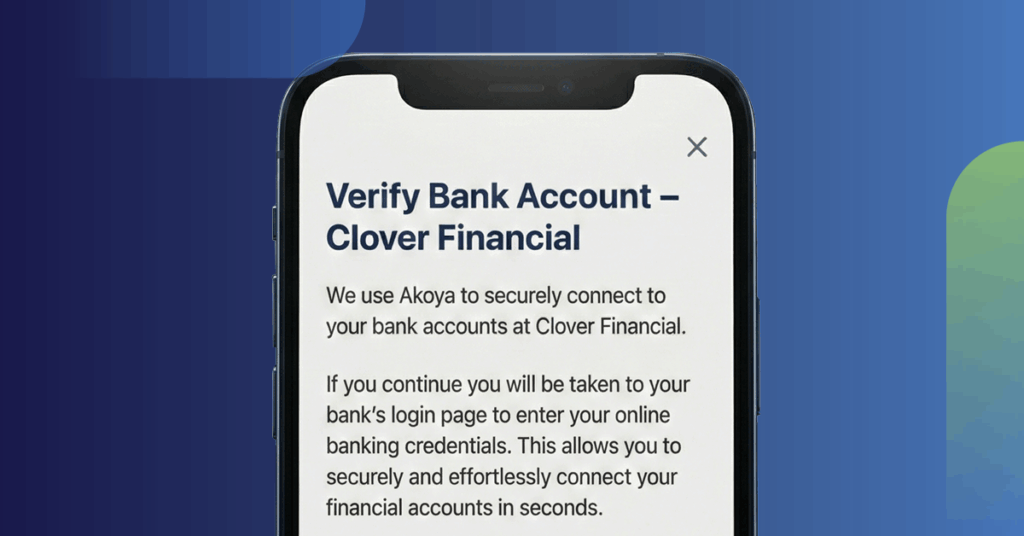

Credential-based verification which represents the most direct confirmation of ownership by using digital banking access to prove account control, though coverage and customer comfort vary by institution.

The growing reliance on instant and same-day payment rails is changing how these methods are evaluated. When payments are expected to post immediately, ownership verification can no longer be treated as a background process. Legacy approaches often force customers to wait. “It could take a few days, especially if the account’s added at the weekend,” Bain said. This increasingly conflicts with how customers expect to transact.

In this environment, ownership verification is becoming a prerequisite for real-time payments rather than an enhancement layered on afterward. Institutions are being pushed to confirm legitimacy the moment a new account is added, not after a payment attempt fails. This shifts verification from a compliance exercise into a core component of payment risk management—one that directly influences customer experience, operational efficiency, and fraud exposure.

An audience member asked whether ownership verification applies only to ACH or also supports wire payments. Bain clarified that verification is not tied to a single rail and can be reused across payment types once an account is verified, describing it as independent of “the underlying payment rail.”

Instant Rails & Verification

Real-time and same-day networks are not just faster alternatives to ACH—they fundamentally change when and how verification can occur. Rather than verifying an account days before a payment is initiated, institutions can now confirm account legitimacy the moment a customer needs to transact.

When a receiving institution supports real-time credit transfers, challenge deposits can be sent and confirmed almost immediately. For the remaining institutions, Same Day ACH serves as a secondary path, enabling verification to occur within the same business day rather than over multiple settlement cycles.

That distinction matters because speed directly affects completion. Legacy challenge deposits, typically sent via ACH, introduce unavoidable lag—especially when accounts are added outside standard processing windows. Bain pointed out that with traditional approaches, verification “could take a few days, especially if the account’s added at the weekend,” creating friction at exactly the moment customers are most motivated to pay.

Instant rails reduce verification delays by providing immediate feedback. When a real-time challenge deposit is sent, institutions can quickly determine whether an account number is valid and reachable. Rejections are identified instantly, while accepted transactions allow verification to continue without forcing customers to wait, giving both institutions and customers fast clarity early in the process.

Credential-based verification further compresses the timeline by confirming ownership through authenticated access to a customer’s digital banking environment. Rather than relying on posted transactions, this approach verifies control directly. Because coverage and customer preference vary, fallback options remain essential. Institutions typically layer verification methods—starting with credentials, moving to real-time rails when needed, and using ACH challenge deposits only as a final step.

The convergence of instant rails and verification has meaningful implications for risk management. Faster settlement eliminates the buffer for post-transaction corrections, shifting accountability to the front of the payment flow and reinforcing the importance of confirming both account validity and ownership before a transaction is initiated.

An audience member asked about verification for the FedNow Service and the RTP network. Bain answered that verification is made possible on real-time payment rails through “network response time,” allowing institutions to confirm acceptance almost immediately.

Another audience member asked how instant rails change the timing of verification compared to traditional approaches. Legacy methods “could take a few days, especially if the account’s added at the weekend,” while real-time rails provide much faster clarity, according to Bain.

The final audience question focused on integrating ownership verification into online and mobile banking without introducing friction. Bain explained that instant verification removes the need to tell customers to “come back in two days,” allowing the entire process to be completed within a single session.

Strategic Benefits for FIs

As verification shifts earlier in the payment lifecycle, its value extends well beyond compliance. Ownership verification—particularly when paired with instant and same-day rails—has become a strategic lever for managing risk, improving operational efficiency, and supporting modern payment experiences without reintroducing friction.

One of the most immediate benefits is risk reduction. By confirming ownership before a payment is initiated, institutions can eliminate many return scenarios tied to incorrect or unauthorized account use, reducing exposure by ensuring the account is open, valid, and controlled by the party initiating the transaction. This front-loaded certainty becomes especially important for higher-risk or highervalue transactions, where failed payments can carry operational and reputational costs.

Verification also transforms how institutions manage fund availability. While ownership verification cannot eliminate the risk of insufficient funds entirely, it allows institutions to narrow the problem set. Bain explained that once ownership and validity are confirmed, institutions are “primarily dealing with the insufficient funds risk at that point in time,” rather than layered uncertainty around account legitimacy. When combined with Same Day ACH or real-time credits, this approach enables faster identification of returns and reduces the need for extended holds or manual review.

From an operational perspective, faster verification supports more self-service payment journeys. Customers can add accounts, confirm ownership, and complete transactions within a single session, eliminating multi-day delays and reducing the need for support intervention. Over time, this shift can:

- Reduce call center volume

- Lower exception handling

- Streamline payment operations

Ownership verification also plays a critical role in customer retention and competitive positioning. As real-time payments become more widely available, customers increasingly expect immediate confirmation and clarity. Institutions that support faster verification signal readiness to support modern payment behaviors. Bain framed this as a visibility issue as much as a technical one, noting that customers recognize when their institution supports newer payment modalities and interpret that support as keeping pace with the market.

For business customers, the stakes are even higher. Industry research (Datos Insights Q1 2024 U.S. Cash Management Survey) shows that concern about payment fraud is widespread, with over 90% of business customers concerned about payments fraud. Despite this high level of concern, verification gaps remain—nearly 38% of businesses still rely on checks due to the lack of comprehensive, Bain was asked by an audience member about tradeoffs between traditional challenge deposits and newer verification approaches. Bain noted that real-time methods eliminate the need for “hard money leaving the institution,” reducing operational overhead and followup work.

Solution Overview

Alacriti offers a standalone, platform-wide service that can be used across multiple payment use cases rather than tied to a single rail or transaction type. Orbipay Bank Account Validation & Verification (BVV) Service is designed to support both compliance-driven validation requirements and higher-assurance ownership verification as payment speeds increase.

Validation

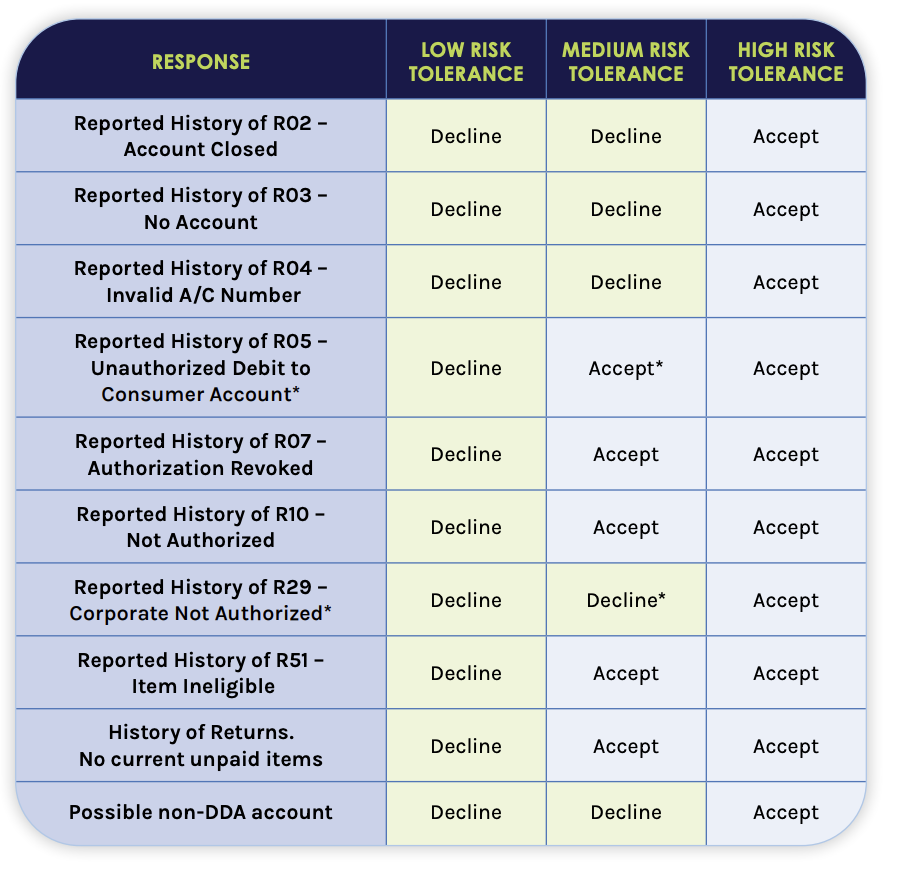

At a baseline level, Alacriti provides bank account validation to support compliance with the Nacha Web Debit Rule, using external data sources to confirm that an account number is structurally valid for a given routing number. A more advanced option extends this capability by returning warning indicators based on adverse account history, such as prior returns, closed accounts, or disputed transactions. This allows financial institutions to define their own risk tolerance and decide whether to accept an account based on more than a simple pass/fail response.

Verification

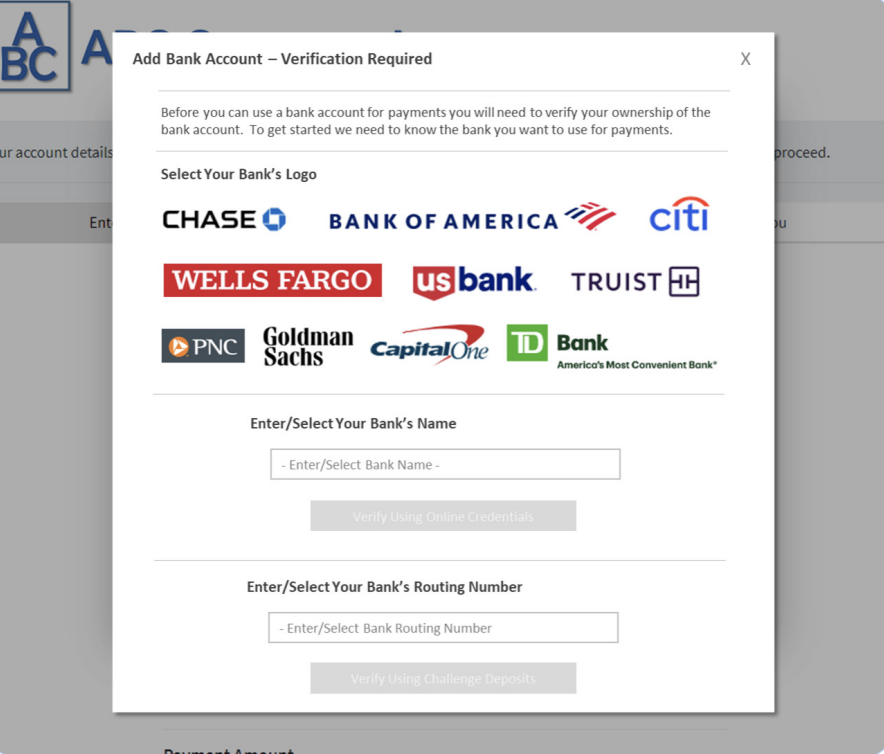

Building on validation, Alacriti has expanded its offering to include ownership verification. Institutions can verify account ownership using multiple approaches, including challenge deposits and credentialbased verification, with logic that prioritizes faster options where available. When a receiving institution supports real-time credit transfers, challenge deposits can be sent immediately, with Same Day ACH used as a fallback for institutions that are not yet enabled. Rather than relying on random micro-deposits, the verification process can use a small-value transaction paired with an alphanumeric code, allowing customers to confirm ownership without guessing transaction amounts.

For credential-based verification, Alacriti integrates with open banking providers to allow customers to authenticate directly with their financial institution. Credentials are not handled by Alacriti; instead, customers are redirected to their bank, and account information is returned through secure tokens. When supported, this approach can return multiple eligible accounts, allowing customers to select which accounts they want to link.

The validation and verification services can be deployed as a fully hosted, turnkey experience or accessed through APIs for institutions that prefer to embed the functionality within their existing digital banking environments. Because the service is decoupled from the payment rail, a verified account can be reused across ACH, real-time payments, wires, and other transaction types.

Beyond account setup, verification checks can be run at the time of payment for higher-risk or higher-value transactions. This ensures that an account remains valid and accessible even if it was originally added years earlier, shifting risk management earlier in the payment flow and reducing exposure to failed or misdirected payments.

The Path Forward for Account Verification

As faster payment rails continue to expand, account verification can no longer operate as a background process or a post-transaction safeguard. The shift toward real-time and same-day payments is forcing financial institutions to move risk decisions earlier in the payment lifecycle, where certainty matters most. Ownership verification, paired with the right mix of instant and fallback rails, is emerging as a foundational capability—one that enables institutions to manage fraud exposure, support self-service digital experiences, and keep pace with rising customer expectations without reintroducing friction.

To learn more about how institutions are strengthening payments risk management as faster rails become the norm, watch the full webinar, Smarter Bank Account Verification, Better Risk Management

Alacriti’s Orbipay Loan Payments is a customizable electronic billing and payments solution for businesses and financial institutions of all sizes. Orbipay Loan Payments offers convenient and flexible choices that include all the payment channels, payment methods, and payment options expected from a modern digital bill pay experience.