The challenge for many institutions is determining how to evolve their payments strategy in a way that meets rising customer expectations while preserving control, flexibility, and compliance.

In an ICBA-hosted discussion, Modernizing Without Disruption: How Community Banks Can Balance ACH and Real-Time Rails, Neeraj Gupta, SVP of Product Management at Alacriti, explored how community banks are navigating payments modernization by supporting ACH and real-time rails in parallel rather than treating them as competing options. The perspectives shared focus on practical considerations shaping payments

strategy today, including when ACH remains the right fit, where real-time payments deliver measurable value, and how centralized orchestration can simplify operations

across rails.

Quick Links

Where Institutions Are Investing Next

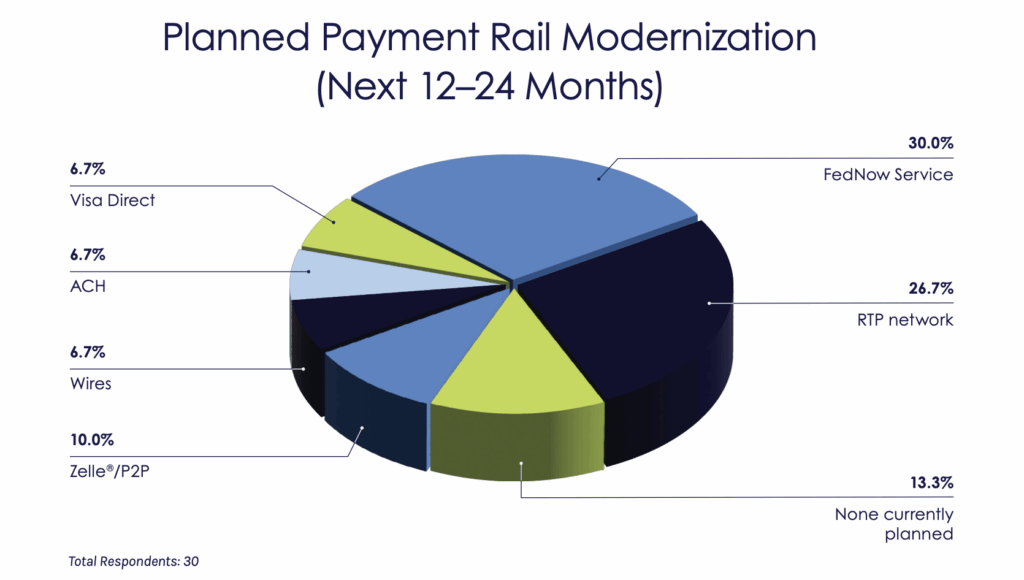

The first poll asked institutions which payment rails they plan to modernize or add over the next 12 to 24 months. The responses point to strong interest in real-time payments, with both major U.S. instant rails drawing attention. 30% of respondents indicated plans to modernize or adopt the FedNow® Service, while 26.7% pointed to the RTP® network, suggesting that many institutions are evaluating both options rather than committing to a single real-time path.

Gupta noted that this dual interest reflects how banks are approaching modernization pragmatically. Rather than treating instant payments as a monolithic capability, institutions are assessing readiness, network coverage, and use cases across networks before making longer-term decisions. He emphasized that this period is less about choosing winners and more about building flexibility as adoption and volumes evolve.

At the same time, the results indicate that modernization is not limited to instant payments alone. Smaller but meaningful portions of respondents cited plans to invest in Zelle® or other P2P services, Visa Direct, ACH, and wires. Gupta shared that this reinforces a broader trend he sees emerging across the market: banks are modernizing payments holistically, recognizing that customer expectations span multiple rails and interaction types. The 13.3% of respondents with no current plans further establishes that adoption timelines vary widely based on institutional priorities and constraints.

Audience Poll: Planned Payment Rail Modernization (Next 12–24 Months)

Modernization Without Disruption

Across the industry, payments are no longer viewed as a back-office utility. Rising customer expectations, increasing transaction volumes, and competitive pressure from fintechs are elevating payments to a strategic priority. Most financial institutions expect payment volumes to continue growing, with few anticipating any slowdown. At the same time, consumers and businesses are increasingly willing to switch providers if their digital experiences fall short, putting added pressure on modernization.

This shift extends well beyond consumer banking. Small businesses and commercial clients increasingly expect the same immediacy and transparency they experience in consumer payment apps. As a result, payments infrastructure is becoming a key determinant of relationship retention, not just operational efficiency.

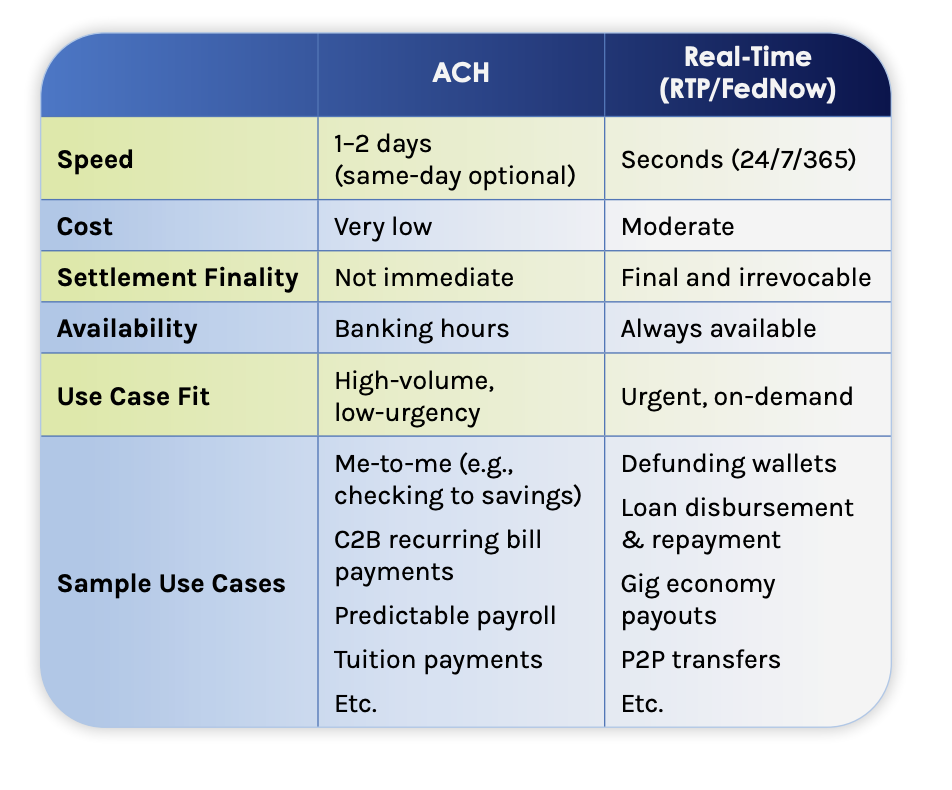

Yet modernization does not imply abandoning ACH. ACH remains deeply embedded in the U.S. banking system and continues to grow in both volume and value, with overall ACH transaction volume up 6.7% year over year and Same Day ACH volumes increasing more than 45.3%. “ACH is not going away,” Gupta said. “It continues to grow and expand into new use cases, even as real-time payments gain traction.” Its scale, predictability, and cost structure make it indispensable for many payment flows.

Real-Time Payments Are Filling a Different Gap

While ACH remains foundational, real-time payments are gaining relevance in scenarios where timing and certainty matter most. Adoption across the RTP network and the FedNow Service has accelerated rapidly, expanding both the number of participating institutions and the range of supported use cases.

One indicator of this shift is when real-time payments occur. Nearly 70% of RTP transactions are initiated outside traditional business hours—well beyond the boundaries of batch-based settlement schedules. “Nearly 70% of [our] real-time payments are happening outside of nine-to-five, Monday through Friday,” Gupta noted.

This behavior highlights the critical role instant payments play in modern liquidity management. Customers are using real-time rails for payroll advances, account funding, wallet transfers, loan disbursements, and other situations where waiting until the next business day is no longer acceptable.

Audience Poll: Where Institutions Are Investing

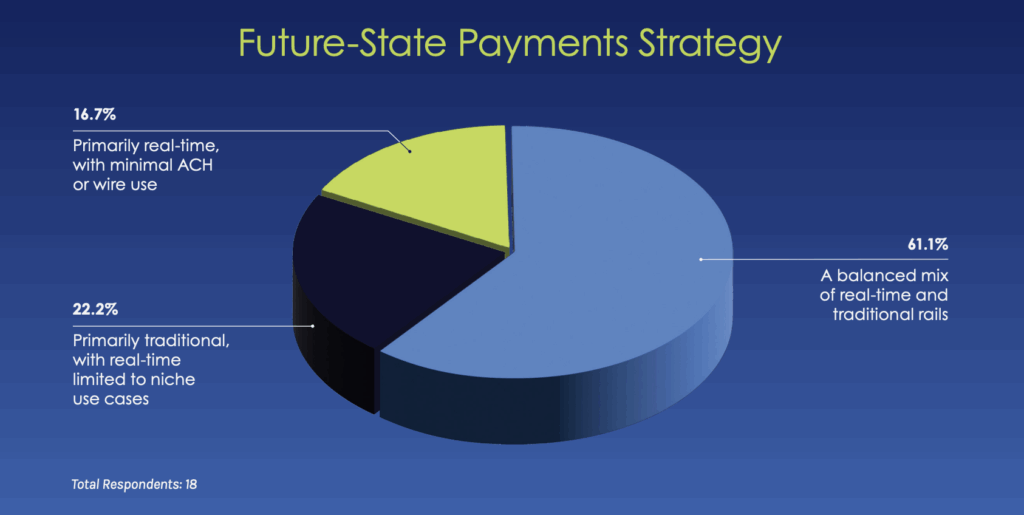

The second poll explored how institutions envision their future-state payments environment. A clear majority—61.1%—reported their goal is a balanced mix of real-time and traditional rails. Another 22.2% expect to remain primarily traditional, with real-time payments applied selectively, while 16.7% indicated a preference for a future state that is primarily real-time.

Gupta observed that this distribution closely mirrors what he observes in community banks today. Most institutions are not pursuing wholesale replacement of ACH or wires. Instead, they are looking to layer real-time capabilities alongside existing rails, aligning each with the scenarios they serve best. This balance reflects both operational realities and customer demand, particularly as ACH continues to grow in volume and value.

He also noted how the smaller group leaning heavily toward real-time payments often has specific use cases driving that position, such as liquidity-sensitive consumer or business flows. At the same time, the continued presence of institutions planning to remain largely traditional shows the enduring role of ACH and wires for high-volume, recurring, and regulated payments. Coexistence—not disruption—is shaping most modernization strategies.

The distribution reinforces a central theme of the discussion: most institutions view real-time payments as a complement to ACH rather than a substitute. Gupta noted that this bell-curve pattern closely reflects what banks are implementing today. “Most institutions see this as a balanced approach rather than an either-or decision,” he said.

Use Cases Should Drive the Rail Decision

A central principle shaping modernization strategies is that payment rails should follow use cases—not the other way around. Each rail is optimized for different conditions, and forcing transactions into the wrong workflow can introduce unnecessary cost or friction.

ACH remains well-suited for high-volume, recurring transactions such as payroll, bill payments, healthcare payments, and predictable account-to-account transfers. These flows benefit from ACH’s efficiency and scale, even as customer expectations around speed continue to rise.

Real-time payments are increasingly used for liquidity-driven, timesensitive scenarios. Emerging data highlights strong activity from digital wallets, cash advance providers, payroll platforms, wealth management firms, and gaming operators. These use cases reflect consumer and business demand for immediate access to funds, particularly outside standard operating hours.

The Hidden Challenge: Legacy Infrastructure

Despite ACH’s continued growth, many institutions are constrained by aging infrastructure. Batch settlement schedules, limited real-time visibility, manual exception handling, and fragmented workflows all drive higher operating costs and can undermine customer experiences.

Legacy systems also hinder an institution’s ability to respond to regulatory scrutiny, fraud risk, and demands for API-enabled access. As real-time expectations rise, these constraints become more visible—not because ACH is inadequate, but because the systems supporting it were not designed for today’s fast-paced payments environment.

Balancing Speed, Stability, Compliance, and Experience

Supporting multiple payment rails introduces complexity across fraud controls, compliance, reporting, and customer experience. Managing each rail independently often results in duplicated rules, inconsistent controls, and operational silos.

To address this, many institutions are adopting a unified orchestration layer that governs payments across rails. This approach allows banks to apply consistent policies while still accounting for the unique characteristics of ACH, real-time payments, and wires. “The rail itself is only one piece of the puzzle,” Gupta explained. “The orchestration layer is what allows you to balance speed, stability, compliance, and user experience across all of them.”

From a customer standpoint, this enables outcome-driven experiences. Rather than navigating separate workflows, customers can be guided by their urgency or cost preference while the system determines the appropriate rail in real time.

Pricing for Value, Not Complexity

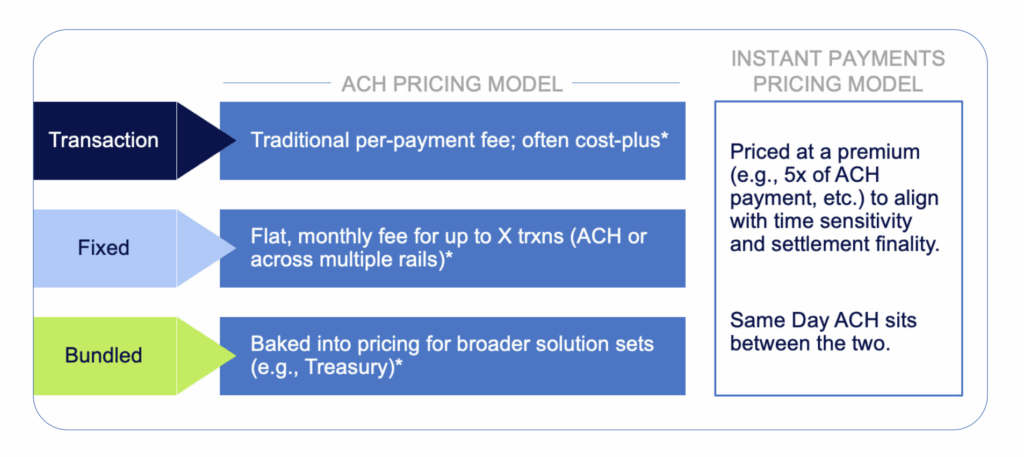

Modernization is also reshaping how payments are priced. ACH pricing models remain largely transaction-based, fixed, or bundled, particularly in treasury and commercial contexts. Real-time payments, however, are increasingly positioned around value-based pricing tied to immediacy and settlement finality.

Institutions are increasingly aligning pricing across rails to present a cohesive experience. “Customers are willing to pay more when speed and certainty truly matter,” Gupta said. Same Day ACH often sits between standard ACH and instant payments, reinforcing a spectrum of choice rather than a binary decision.

Use Value-Based Pricing for Instant Rails to Complement ACH

What Modernization Looks Like in Practice

Real-world examples demonstrate how these strategies come together in practice. One institution described deploying an omni-rail model with centralized fraud controls, exception management, reporting, and real-time posting.

Within the first month, the bank processed more than $1 billion across multiple geographies, with activity spanning over ten countries. Centralized configuration reduced manual effort and improved visibility, allowing staff to focus less on maintaining rails and more on higher-value work. “Centralization allowed them to focus less on maintaining rails and more on serving customers,” Gupta said.

ACH and Real-Time Payments Will Coexist

A common industry question is whether legacy rails will eventually fade out. The prevailing view is that ACH will remain central for the foreseeable future. “On a five-to ten-year horizon, I don’t see ACH going away,” Gupta said. “Its stability is a big part of why it remains central to the system.”

At the same time, institutions that delay real-time adoption risk falling behind customer expectations. Modernization without disruption requires recognizing that both ACH and real-time payments have distinct roles—and that value is created by aligning them intelligently.

To learn more about how community banks are modernizing payments while preserving stability, watch the full webinar, Modernizing Without Disruption: How Community Banks Can Balance ACH and Real-Time Rail

Alacriti’s centralized payment platform, Orbipay Payments Hub, provides innovation opportunities and the ability to make smart routing decisions at the financial institution to meet their individual needs. Financial institutions can take full ownership of their payments and control their evolution with TCH’s RTP® network, the FedNow® Service, Zelle®, Fedwire, ACH, and Visa Direct, all on one cloud-based platform.

Zelle® and the Zelle® related marks are wholly owned by Early Warning Services, LLC and are used herein under license.