Modernizing payments is no longer a choice for large financial institutions—it’s an operational and strategic necessity. As real-time payments gain momentum, banks must find ways to preserve the reliability of ACH while integrating faster rails, such as the RTP® network and the FedNow® Service.

In the American Banker–hosted webinar Bridging the Gap Between ACH and Real-Time Payments, Neeraj Gupta, SVP of Product Management at Alacriti, shared how leading institutions are intelligently orchestrating ACH and instant payments to optimize routing, support diverse use cases, and generate new revenue opportunities.

Quick Links

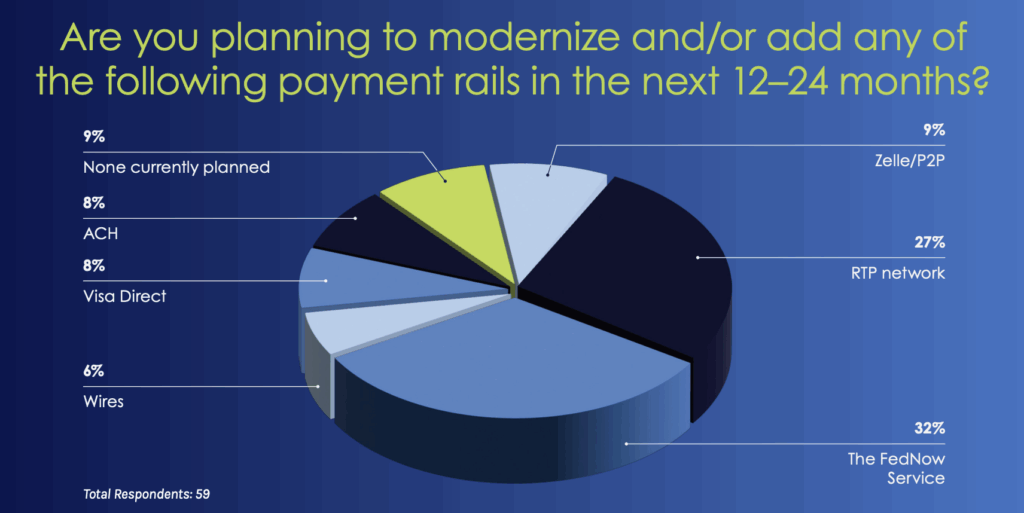

Audience Poll Question: Payment Rail Modernization Plans?

The session began with a live audience poll exploring which payment rails financial institutions plan to modernize or add over the next 12 to 24 months. The results revealed a strong push toward real-time payments: 32% of respondents selected the FedNow Service and 27% chose the RTP network, representing nearly 60% of all responses. Other selections included Zelle®/P2P (9%), Visa Direct (8%), ACH (8%), Wires (6%), and None currently planned (9%).

The results illustrated that instant payments are taking center stage in modernization strategies for financial institutions. Realtime rails like RTP and FedNow are quickly emerging as table stakes for institutions aiming to meet the speed, transparency, and 24/7 availability expectations of today’s customers.

Modernization Without Disruption

For financial institutions, the challenge of modernizing payments isn’t simply about adopting new rails—it’s about doing so without disrupting the systems that already serve as their foundation. As consumer expectations rise and transaction volumes accelerate, banks and credit unions must rethink their approach to innovation while maintaining reliability, speed, and member satisfaction.

Consumer behavior is driving much of this urgency. With 76% of consumers likely to switch banks if they find one that better meets their needs (up from 52% in 2020), financial institutions must act decisively to meet emerging challenges and seize new opportunities. The message is clear: customers expect seamless, intuitive, and real-time interactions—and they’re willing to leave institutions that fail to deliver them.

According to Datos Insights, “An overwhelming 96% of banks are making significant investments in payments modernization, recognizing the critical nature of this transformation.” Much of that investment is focused on overcoming legacy, siloed, fragmented technology that slows down innovation and prevents financial institutions from meeting demand efficiently.

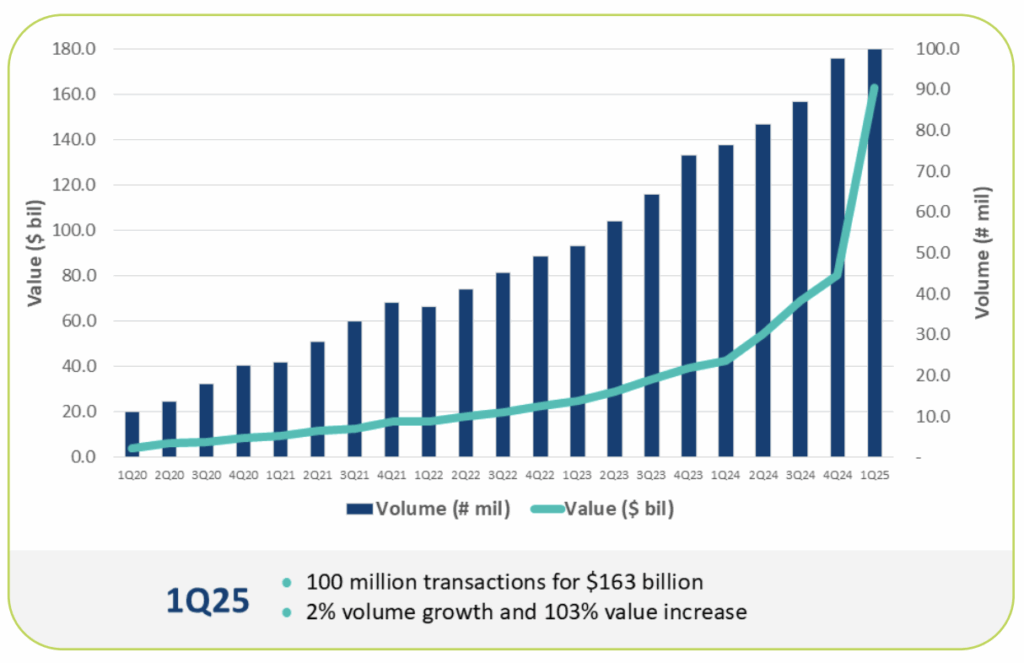

At the same time, the evolution of payment networks is reshaping how modernization takes place. “The RTP network has matured into what is described as a story of growth, the landing has taken place— it’s more about expansion,” Gupta shared. According to The Clearing House, the RTP network processed nearly $250 billion in 2024 and is approaching one million transactions a day. Meanwhile, the FedNow Service, still in its early stages, is focused on onboarding participants— about 1,500 participants and 40 different service providers—as it builds toward scale.

Yet modernization doesn’t mean abandoning ACH. “The ‘powerhouse’ of U.S. payments, ACH, is not going away. It’s actually growing,” Gupta emphasized. Overall, ACH volume rose almost 7% year-over-year, with Same Day ACH up almost 50%.

Yet modernization doesn’t mean abandoning ACH. “The ‘powerhouse’ of U.S. payments, ACH, is not going away. It’s actually growing,” Gupta emphasized. Overall, ACH volume rose almost 7% year-over-year, with Same Day ACH up almost 50%. The real challenge, he said, lies in “keeping up with that volume in an operationally efficient, memberpleasing way,” especially when legacy systems slow time to market and limit flexibility.

Despite ACH’s continued dominance—moving more than $86.2 trillion in 2024—it remains constrained by legacy systems that are decades old. Much of today’s ACH infrastructure still relies on batch processing and manual workflows, creating operational fragility and driving up costs. As volumes rise and Same Day ACH adoption accelerates, financial institutions face mounting pressure to deliver real-time availability and greater transparency without the benefit of real-time infrastructure. At the same time, growing regulatory scrutiny and demand from fintechs for API-enabled access are exposing the limits of outdated systems. The result is widening the gap between ACH’s reliability and the innovation required to keep pace with modern expectations—a gap many institutions are now seeking to close through modernization.

Ultimately, modernization without disruption requires a balanced strategy, one that leverages instant payments to meet new expectations while optimizing the traditional rails that still move the majority of transactions. Success will come not from choosing between ACH and real-time payments, but from intelligently orchestrating to deliver a seamless, always-on payments experience.

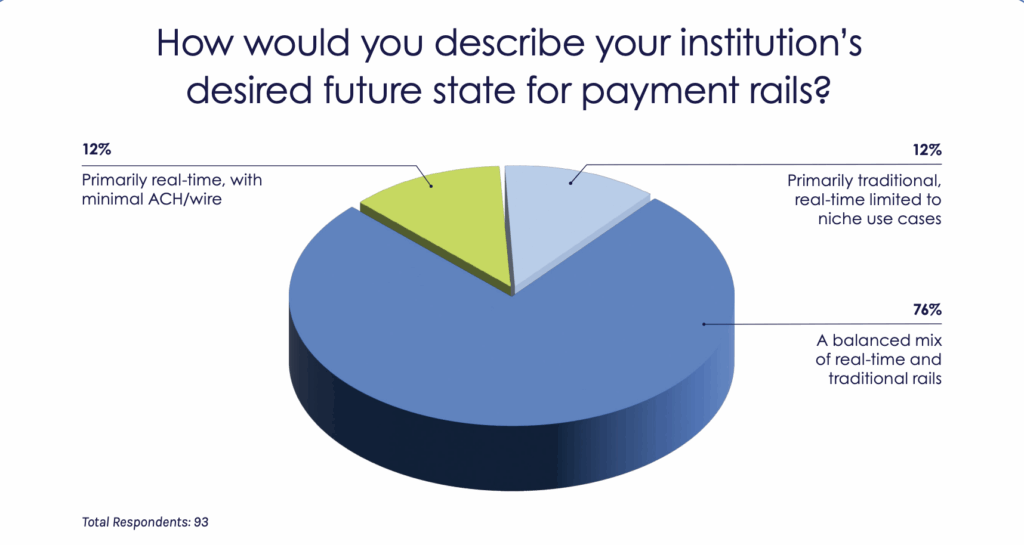

Audience Poll Question: The Future State of Payment Rails

The second audience poll asked participants how they envision their institution’s future state for payment rails. The results revealed strong consensus around balance rather than replacement. A majority (76%) indicated that their goal is to maintain a balanced mix of real-time and traditional rails, while just 12% selected primarily real-time with minimal ACH or wire use, and another 12% said they expect to remain primarily traditional, with real-time limited to niche use cases.

The findings suggest that most financial institutions view modernization as an additive—not disruptive—journey. Rather than choosing between legacy systems and instant payments, banks and credit unions are aiming to integrate both to serve diverse use cases and customer segments.

That mindset reflects the industry’s growing recognition that no single rail can meet every need. While real-time payments are essential for speed and innovation, ACH and wires continue to provide scale and reliability. Together, they form the backbone of a payments ecosystem that allows institutions to modernize strategically—without sacrificing stability or customer experience.

Strategic Use Case Alignment

Modernizing payments isn’t just about adopting faster rails—it’s about understanding where and when to use them. The most forwardthinking financial institutions are no longer asking whether they need real-time payments; they’re asking how to align each payment rail with the right strategic use cases to maximize both customer value and business opportunity.

“This is not theoretical, this is empirical,” Gupta explained. Drawing on data from Alacriti’s client portfolio, he outlined how different types of payments—ranging from digital wallet defunding to payroll and gig economy disbursements—are revealing clear behavioral trends. For example, “20% of the dollars coming into our FIs for instant payment rails came in from PayPal, Venmo, Cash App, etc., 25% by count came in from those.” These smaller, frequent transactions point to the growing role of real-time payments in supporting liquidity and day-today cash flow.

This insight is already shaping actionable strategies. “If my volume is significantly higher than that of the benchmark,” Gupta said, “Perhaps there’s an opportunity for me to offer short-term lending rather than having some of your accountholders having to go across the street, or go to a Fintech.” By analyzing where real-time payments are concentrated—such as consumer cash flow, business cash flow, or wealth management—institutions can uncover gaps and design new services that strengthen customer retention within their ecosystem.

At the same time, the analysis reinforces that traditional rails like ACH remain essential for predictable, high-volume transactions.

Predictable payments like utilities, tuition, and payroll continue to align with ACH, while real-time payments excel in on-demand scenarios like funding wallets, gaming, and gig disbursements.

Successful payment modernization depends not on replacing rails but on orchestrating them intelligently. By mapping the right use cases to the right payment type, financial institutions can enhance liquidity, improve customer satisfaction, and drive noninterest income—without adding operational complexity.

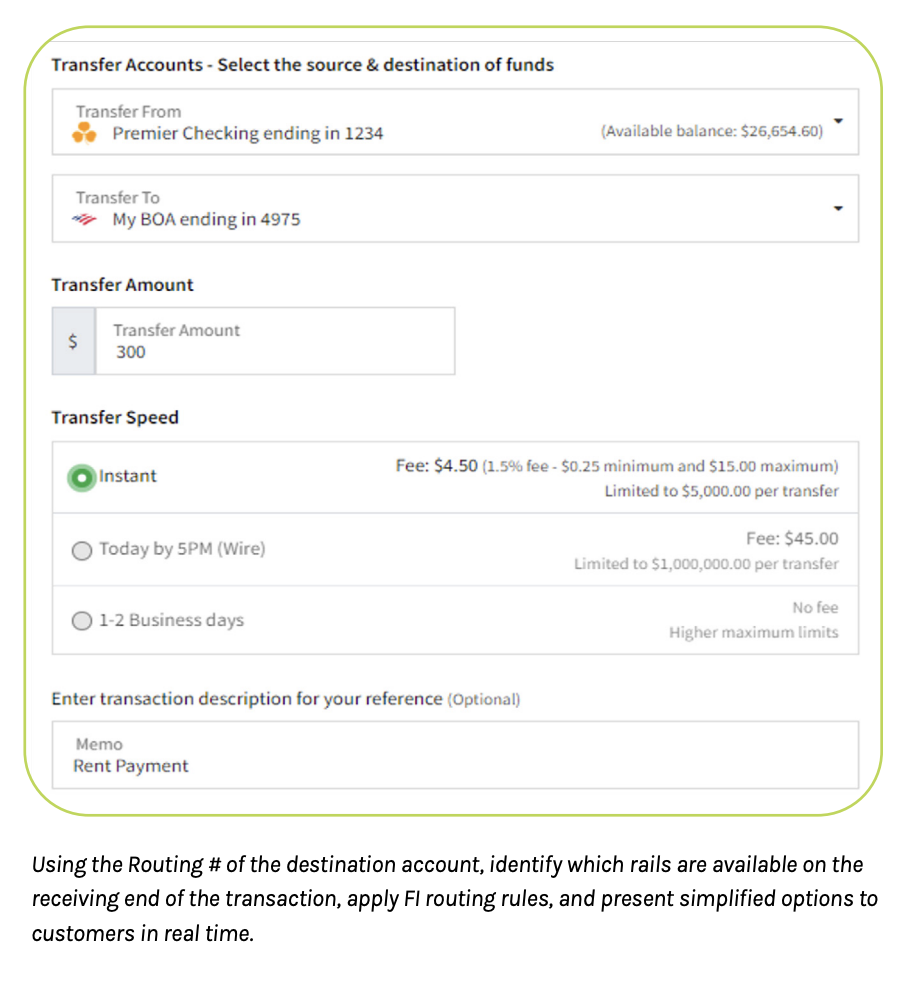

Smart Routing and Infrastructure Readiness

With real-time, ACH, and wire transactions operating side by side, the institutions leading the way are investing in modern infrastructure designed to dynamically route payments, optimize cost and speed, and deliver consistent, reliable outcomes across every channel.

A modern payments hub lies at the center of this transformation. “A central payments engine or payments hub offers quite a bit more than purely an unintelligent pipe out to each of the rails,” Gupta explained. Instead, it serves as a configurable engine that unifies policies, processes, and payment lifecycles under one intelligent framework. This architecture supports everything from fraud and risk management to CRM and digital banking integration—creating a foundation for agility and innovation.

The concept of smart routing exemplifies this evolution. “Everybody uses the example, sort of [like] the UPS model,” Gupta said. “You tell me when you need it to be there, I’ll tell you how to do it—whether it’s boat, rail, auto, plane, whatever it is.” In payments, that means allowing senders to define their priorities—speed, cost, destination, or currency—while the system automatically determines the optimal route.

By enabling this kind of intelligent decision-making, a unified payments hub empowers financial institutions to deliver flexibility without adding complexity. The result is infrastructure that doesn’t just support new rails but strategically orchestrates them—helping banks and credit unions move from fragmented systems to smart, scalable ecosystems built for the future of money movement.

Revenue Opportunities and Pricing Models

As instant payments become mainstream, financial institutions are rethinking how to price and position them—not just as a cost center, but as a source of value. Modern pricing strategies are evolving beyond traditional transaction-based fees to reflect the premium customers place on speed, certainty, and convenience.

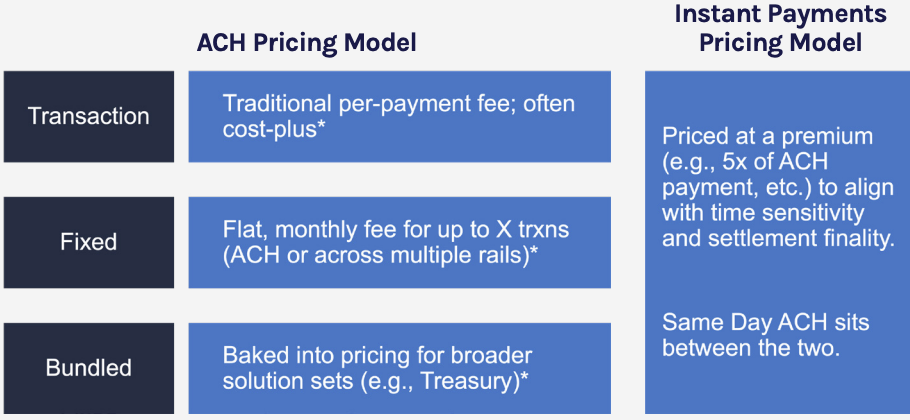

Across the market, several models have emerged. “A couple of different models—either on a per-transaction or per-click, a fixed sort of all-you-can-eat or bundled, especially when we’re getting into the commercial space,” Gupta explained. Many institutions continue to package ACH and treasury solutions together for simplicity, but the addition of instant payments introduces new dynamics—and new opportunities to align pricing with value,

“What we’ve seen the most successful FIs do is to not price them in silo fashion, but in complementary, cohesive fashion in order to align cost or align pricing to value,” Gupta shared. In practice, that often means applying a modest premium for instant payment rails such as the RTP network and the FedNow Service. Many banks have found that “FedNow and RTP transactions [are] being charged five times [ACH],” while same-day ACH might be ‘two or three times,’ creating a logical, more transparent structure for clients.

This value-based approach not only reflects the enhanced utility of real-time payments but also helps financial institutions position instant rails as a differentiator rather than a commodity. By offering clear, tiered pricing models tied to business outcomes, banks and credit unions can capture new revenue streams while educating customers on the tangible advantages of speed in payments.

Common ACH Pricing Models

Value-Based Pricing for Instant Rails to Complement ACH

Real-World Insights

While payment modernization often sounds theoretical, real-world results highlight how a unified payments infrastructure can drive measurable impact. One Midwestern bank Gupta cited as an example recently demonstrated the power of a centralized payments hub— integrating instant payments, wires, and ACH within a single intelligent framework to enhance scalability and efficiency.

“One of the promises of this centralization is I can control my fraud and risk, AML, sanction screening, etc., from one place such that every new rail just becomes a slight incremental bit of effort on top of that,” Gupta said. By consolidating controls and integrations, the institution was able to expand from real-time payments to wire transfers with minimal additional effort—proving that modernization doesn’t have to come with disruption.

The same efficiencies extended to exception management and ecosystem integrations. “They were able to leverage a lot of that already configured precise policy and set of vendor plumbing they already had in place,” Gupta said. This approach streamlined operations, enabling the bank to scale quickly and add new payment capabilities without reinventing its technology stack each time.

Even within instant payments, intelligent routing played a crucial role. For example, the institution could automatically determine when a transaction should route over the FedNow Service versus RTP based on factors like funding and availability. This “behind-the-scenes logic” helps financial institutions optimize performance while maintaining flexibility across multiple rails.

An audience question revealed that many institutions are implementing the RTP network and the FedNow Service with Alacriti in tandem, often starting with receive on both rails and then adding send. As Gupta explained, “They often will do both rails at the same time, whether that means starting with receive on both rails and then moving on to send on both rails.” The reasoning is clear—much of the operational, educational, and compliance work applies across both networks. “When 80% of the message is the same, they’re often doing those at the same time,” Gupta said, noting that this approach aids in streamlining internal training and accelerating adoption.

Recommended Strategy

Winning institutions aren’t choosing between ACH and instant payments—they’re intelligently orchestrating both. By centralizing controls, rolling out RTP and FedNow in parallel, and using smart routing to align each rail with the appropriate use case, banks can deliver 24/7 speed without sacrificing reliability or compliance. Layering value-based pricing then turns real-time capabilities into measurable business outcomes. With a unified payments hub as the foundation, modernization becomes incremental, scalable, and fully aligned to the way customers move money today.

To learn more about how proactive digital outreach can improve

payment performance, reduce costs, and strengthen customer

loyalty, watch the full webinar, Shifting the Payments Paradigm: Why

Digital Outreach Matters to Your Bottom Line.

Alacriti’s Loan Payments, is a customizable electronic billing and payments

solution for businesses and financial institutions of all sizes. Orbipay EBPP

offers convenient and flexible choices that include all the payment channels,

payment methods, and payment options expected from a modern digital bill

pay experience.

Zelle® and the Zelle® related marks are wholly owned by Early Warning Services, LLC and are used herein under license. To send or receive money with Zelle®, both parties must have an eligible checking or savings account.