Credit unions are consistently looking for ways to modernize bill pay, reduce friction, and meet members’ expectations for faster, more intuitive digital experiences. With real-time payments gaining momentum and new use cases emerging across the RTP® network and the FedNow® Service, Request for Payment (RfP) is becoming a pivotal tool for improving convenience, streamlining loan and bill payments, and

strengthening member engagement.

In a Callahan-hosted session, Beyond Bill Pay: Using RFP and Real-Time Payments To Deepen Member Relationships, Stuart Bain and Mark Majeske explored how RfP is evolving, how it connects to broader real-time payment strategies, and why it’s poised to reshape how credit unions support account funding, recurring bills, and payment approvals across channels.

Quick Links

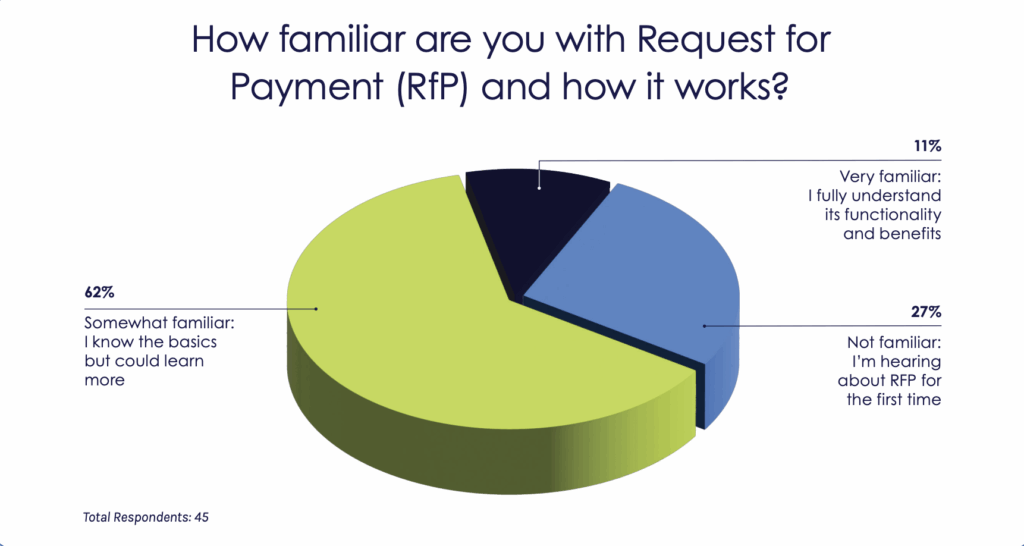

Audience Poll: How Familiar Are Credit Unions With RfP?

To ground the discussion, the webinar opened with a poll asking credit union attendees how familiar they were with Request for Payment (RfP). The results showed just how early the industry still is in adopting—and even fully understanding—this capability. Out of 45 respondents, 62% indicated they were “somewhat familiar” with RfP, while 27% were hearing about it for the first time. Only 11% reported being “very familiar” with its functionality and benefits.

This distribution aligns with what Alacriti’s product team sees across the market: most institutions recognize the concept, but few have explored how RfP works on the RTP network or the FedNow Service, or what it can unlock for member engagement, loan payments, and account funding. “It’s early in the game, but these institutions are coming up with some very good and innovative ideas on how to use RfPs,” Majeske noted.

The poll results reinforce why education remains essential. Many credit unions are familiar with RfP-adjacent experiences—such as Pay By Text, CSR Bill Notifications, or P2P request flows in banking apps like Zelle® and consumer payment apps PayPal—but haven’t yet connected those behaviors to what real-time RfP can deliver through the credit union’s own digital channels.

The Industry Is Shifting Toward Real-Time, MemberCentered Payments

Credit unions are entering a pivotal moment in the evolution of bill pay. While digital channels have grown, member behavior shows a clear preference for immediate, mobile-first interactions and transparent, good-funds payments. Traditional bank bill pay continues to decline as 76% of consumers now go directly to the biller for more flexible, on-demand payment experiences—a major factor reshaping how credit unions must approach engagement. At the same time, realtime networks are expanding rapidly. At the time of the webinar, the RTP network supported over 1,000 institutions and recently increased its transaction limit to $10 million, while FedNow adoption continued to climb among credit unions and community banks.

These shifts are converging with generational expectations. Younger members overwhelmingly prefer alerts, mobile prompts, and digital payment flows that require minimal effort—mirroring the convenience they use daily through apps like PayPal, and Venmo. This is setting a new baseline for what “good” looks like in the payment experience, especially when members are managing loan payments, recurring bills, or one-time obligations. “What we’re seeing is this convergence of information that’s held from the perspective of a biller starting to be able to be used as part of the RfP network to streamline that payment experience and make for a much better payment experience across the networks,” Bain explained.

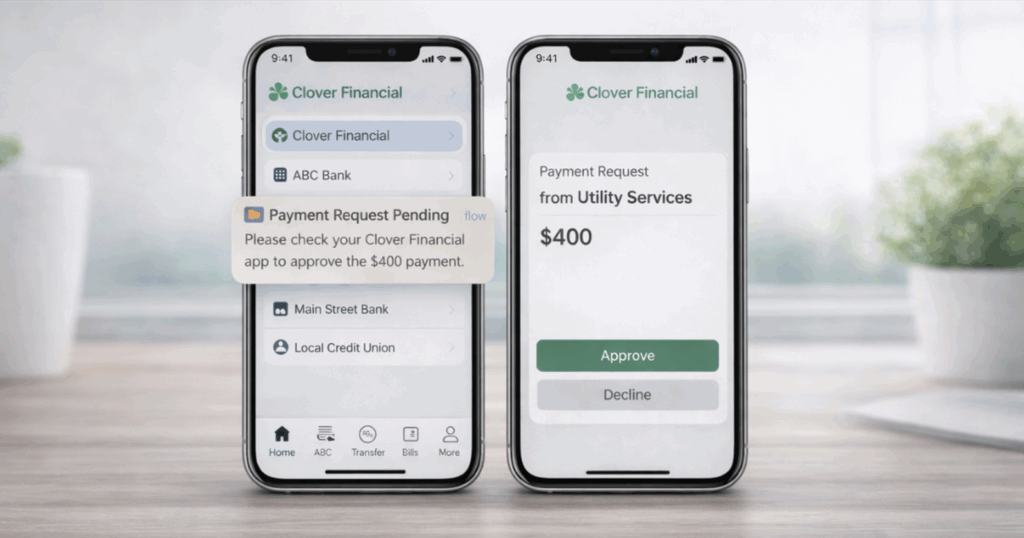

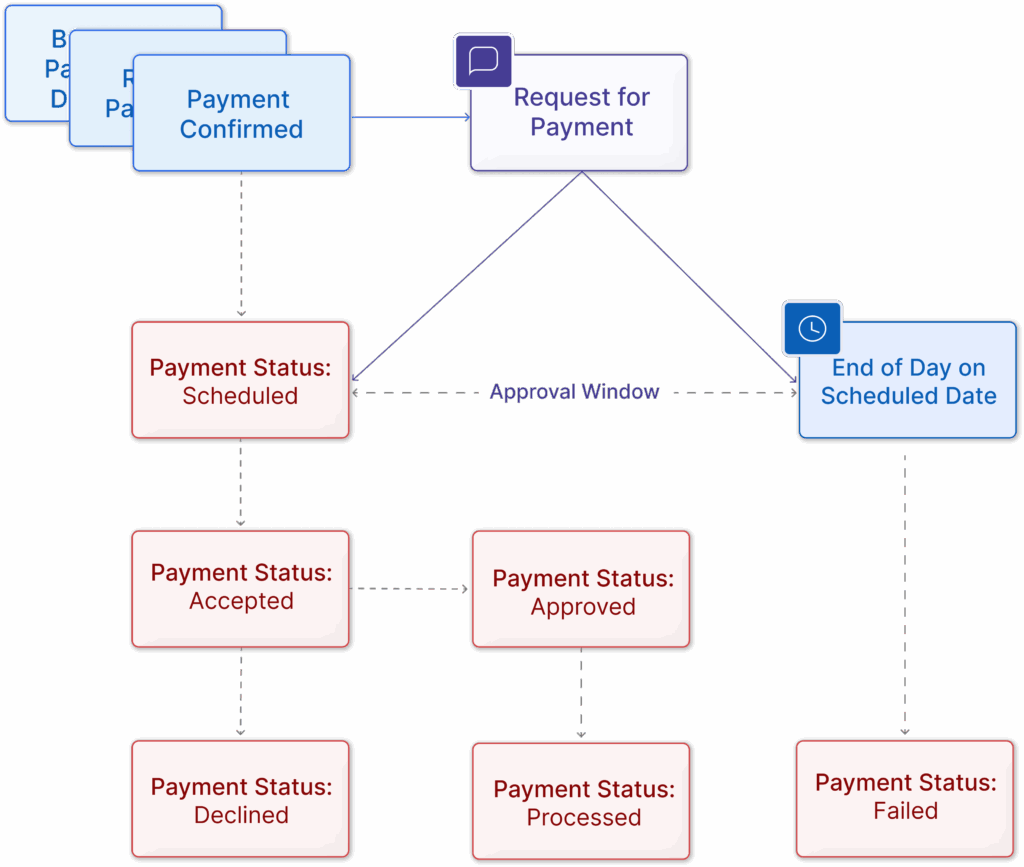

How Request for Pay Works Today

RfP is still early in its market adoption, but its underlying workflow is already proving to be a powerful extension of the real-time payment rails credit unions are adopting. Unlike traditional ACH debits, an RfP is a two-step, member-verified process:

STEP 1

The credit union sends a detailed request

STEP 2

The member must explicitly approve it within their authenticated digital banking experience

This structure introduces a new level of transparency and control, ensuring that members understand exactly what they are paying—and giving credit unions immediate confirmation that the funds are both good and irrevocable.

During the webinar, Majeske outlined how RfP behaves across both the RTP and FedNow networks, emphasizing that the process is identical regardless of rail. Once a request is initiated—whether self-service, system-generated, or CSR-driven—the receiving institution validates the account, alerts the member, and presents clear options to approve, decline, or let the request expire. This creates a more modern, mobile-friendly flow that mirrors the approval experiences members already know from consumer apps.

Adoption today is strongest in use cases such as Account-to-Account (A2A) Transfers and brokerage funding. But RfP’s structure makes it well-suited for a wide range of credit union scenarios—from loan payments to collections reinforcement to time-sensitive transactions like auto purchases or property closings.

One of the key advantages credit unions gain is real-time validation. Because members must authenticate and approve the transaction at their bank, RfP inherently confirms account ownership and available funds. This eliminates the uncertainty around ACH returns and reduces operational risk tied to high-value or urgent payments. The expiration window built into the request also ensures that payments aren’t approved after the amount due has changed—a safeguard traditional channels simply cannot provide.

While current live deployments remain limited compared to the number of institutions certified for RfP, pilots across the networks are accelerating. Importantly, this capability is not reserved for large banks. Credit unions of all sizes are beginning to explore use cases where real-time certainty, member-directed approval, and reduced processing friction can meaningfully improve both experience and outcomes.

As more digital banking providers build native RfP interfaces and notifications, the approval steps will become even more intuitive. For now, credit unions are encouraged to evaluate where two-step, real-time approvals could replace higher-risk or higher-cost payment methods—and where RfP can create a more streamlined, membercentered journey.

RfP in Action

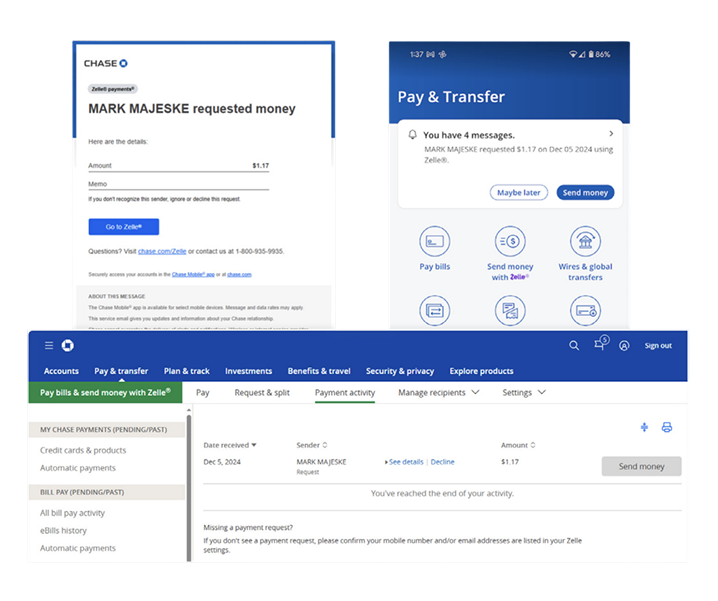

While RfP is still emerging on the RTP network and FedNow Service, members are already familiar with the concept through everyday experiences. Bain and Majeske emphasized that some of the strongest signals of future RfP adoption come from the tools members already use—PayPal, Venmo, Cash App, and especially Zelle®. These platforms have long normalized sending and receiving payment requests, conditioning members to expect simple, two-step approvals. That familiarity creates a bridge for credit unions as formal RfP capabilities begin to scale across real-time networks.

Bain explained how this consumer behavior translates into practical member expectations. When he showed how a Zelle® request displays in Chase’s mobile app—with email alerts, text notifications, and an in-app prompt—he noted how similar the member experience will need to be for RTP and FedNow-based RfPs to succeed. Members must instantly understand when a request arrives, what it’s for, and how to approve it. Digital banking providers will play a key role in ensuring these interactions are intuitive, visible, and secure.

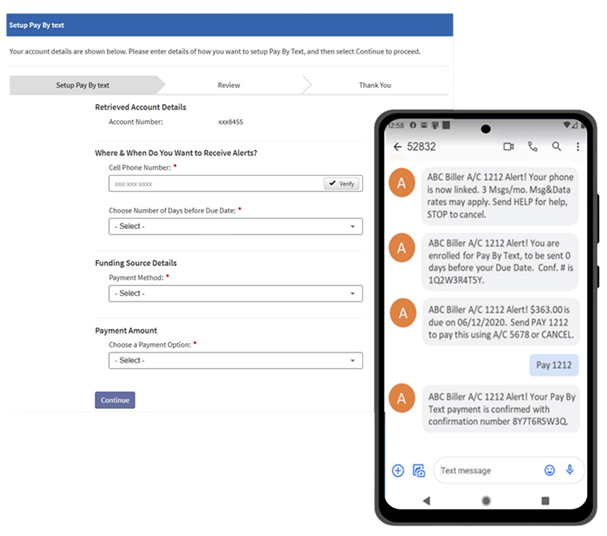

Beyond consumer P2P experiences, credit unions are already using RfP-like workflows in adjacent solutions today. Pay By Text mirrors the same two-step approval model: a member receives a prompt with the amount due, then taps to approve the payment. CSRgenerated notifications—where staff send secure, one-time “magic links” for members to authorize payments—follow the same pattern. Both examples demonstrate that members are already comfortable receiving a prompt and explicitly approving the transaction, even if they don’t yet recognize it as RfP.

This existing behavioral foundation sets the stage for broader, network-driven RfP adoption. “The majority of RfP transactions are A2A between banks and brokerage firms… a lot of people use that for me-to-me transactions, moving funds to and from brokerage accounts,” Majeske noted.

What Would an RFP Payment Flow Look Like?

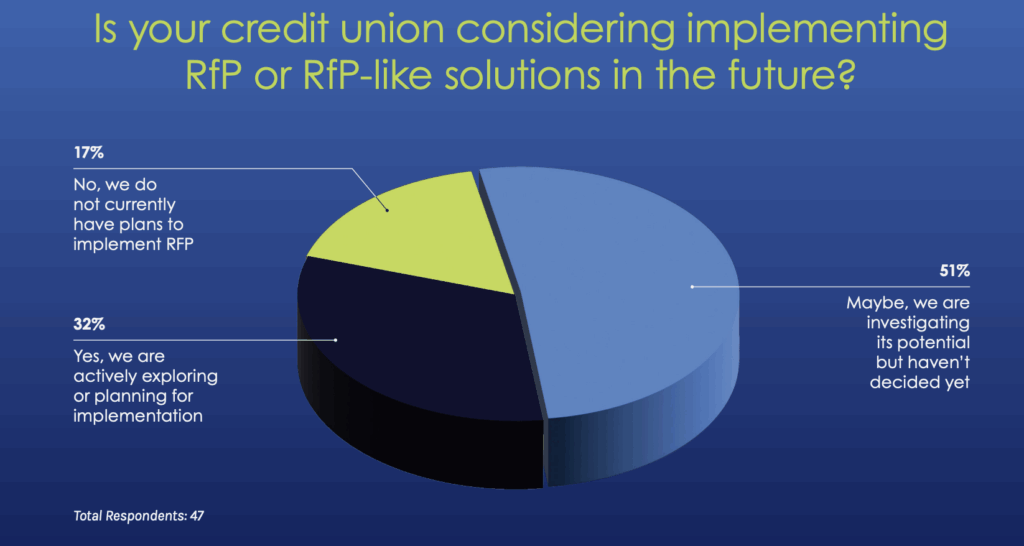

Audience Poll: Are Credit Unions Planning to Implement RfP?

To gauge where credit unions stand on the path toward real-time payments innovation, the webinar included a second audience poll asking whether institutions were considering implementing RfP or RfP-like solutions. The responses revealed a strong and growing appetite for modernization: 32% of attendees reported they are actively exploring or planning for implementation, while an additional 51% said they are evaluating RfP’s potential but have not yet made a decision. Only 17% indicated they currently have no plans to adopt RfP.

This distribution implies that most credit unions recognize that RfP is no longer an abstract, future-state capability, but an emerging tool with real strategic value. The majority are already in the exploratory or evaluative phases. As Mark Majeske noted in the discussion, institutions of all sizes are beginning to participate: “It’s early in the game, but these institutions are coming up with some very good and innovative ideas on how to use RfPs.”

What’s Next for RfP?

The Clearing House and the Federal Reserve continue to refine the RfP message set, expanding support for more sophisticated interactions such as invoice adjustments, recurring approvals, and pre-scheduled requests tied to due dates. Industry working groups are also collaborating on a critical piece of the ecosystem: creating a consistent member experience across receiving institutions. As Majeske explained, one of the biggest challenges ahead is ensuring that “You want to be able to send it to anyone at any bank and have the same user experience.”

This standardization will play a major role in scaling adoption. Once members know where to find RfPs in online banking—and how to approve or question them—credit unions can begin using RfP for more complex or time-sensitive scenarios. The networks are already testing expanded use cases across industries, including real estate transactions, COD deliveries in transportation, and utility shutoff avoidance. Each of these demonstrates how RfP can reduce risk, accelerate decision-making, and eliminate the friction associated with traditional transfers like wires, mailed statements, or next-day ACH.

Credit unions, in particular, are well-positioned to lead the next wave of deployment. With strong member relationships and a wide range of payment-driven journeys—from loan funding to collections to account opening—RfP offers a way to deliver immediate value across multiple touchpoints. As network capabilities expand and digital banking providers integrate native RfP approval flows, the opportunity will shift from experimentation to everyday, seamless usage.

What comes next is not just broader access to RfP but deeper integration into the digital experiences members rely on most. Credit unions that begin exploring use cases now will be better equipped to simplify high-value transactions, reduce risk, and deliver the real-time convenience members increasingly expect.

Strategic Benefits for Credit Unions

Beyond its technical advantages, RfP fundamentally changes how institutions manage risk, support members, and differentiate themselves.

Guaranteed Funds

One of the most significant benefits is the ability to offer guaranteed, irrevocable funds—a major step forward from traditional ACH. For highrisk or high-value scenarios such as delinquent loans, account funding, or property-related transactions, RfP eliminates the uncertainty credit unions face when relying on ACH returns or card disputes. Members must authenticate and explicitly approve the request through their bank, making the funds immediately available and dramatically reducing exposure. This removes the need for holds, manual monitoring, or follow-up calls that strain staff resources.

Meet Member Expectations for Immediacy and Convenience

RfP also strengthens the member experience with modern, mobilefriendly interactions. Instead of waiting for mailed statements or navigating portal-only journeys, members receive a clear, actionable request that mirrors familiar payment flows from Zelle®, Venmo, and PayPal. This familiarity helps credit unions meet rising expectations for immediacy and convenience—especially among younger members who expect streamlined, alert-driven engagement. As Stuart Bain emphasized, supporting real-time payment networks signals innovation: members can see that “Your institution is supporting these new payment networks and these new payment modalities, which means you’re keeping up with the cutting edge of what’s actually out there.”

Lower Operating Costs

Operationally, RfP can lower processing costs by replacing expensive card-funded payments and reducing the need for paper checks, mailings, or manual collections outreach. Whether it’s funding a new CD, resolving a past-due auto loan, or delivering a time-sensitive payoff, RfP shortens the payment cycle and enables credit unions to streamline staff workflows without sacrificing accuracy or security.

Differentiation

Finally, RfP offers a path to meaningful differentiation. As more fintechs embed seamless payment experiences into their applications, credit unions must deliver similar—and often superior— real-time interactions to protect primary financial relationships. RfP gives institutions a way to stand out, offering members speed, certainty, and transparency that directly reinforce trust and loyalty.

Credit unions looking to bring these strategic benefits to life can leverage Orbipay Payments Hub to easily connect to real-time payment rails and activate Request for Payment (RfP) capabilities. With a single integration point and a unified approach to modern money movement, Orbipay Payments Hub empowers institutions to deliver faster, more secure, and more intuitive payment experiences that meet rising member expectations.

To dive deeper into how RFP and real-time payments can modernize bill pay, strengthen member engagement, and reduce payment risk, you can watch the full webinar, Beyond Bill Pay: Using RFP and RealTime Payments To Deepen Member Relationships.

Alacriti’s centralized payment platform, Orbipay Payments Hub, provides innovation opportunities and the ability to make smart routing decisions at the financial institution to meet their individual needs. Financial institutions can take full ownership of their payments and control their evolution with TCH’s RTP® network, the FedNow® Service, Zelle®, Fedwire, ACH, and Visa Direct, all on one cloud-based platform. Alacriti’s Orbipay Loan Payments is a customizable electronic billing and payments solution for businesses and financial institutions of all sizes. Orbipay Loan Payments offers convenient and flexible choices that include all the payment channels, payment methods, and payment options expected from a modern digital bill pay experience.

Zelle® and the Zelle® related marks are wholly owned by Early Warning Services, LLC and are used herein under license.