The demand for speed, efficiency, and user-friendly experiences is reshaping expectations for financial institutions. In a Banking Exchange-hosted webinar, Optimizing Payment Rails: Smarter Solutions for Efficient Money Movement, industry experts Paul Steinbrecher, Director of Payments Consulting at Alacriti, and Jeff Bucher, former Senior Product Manager at Alkami, explored how smart routing and multi-rail optimization are helping institutions rise to the challenge. They also shared a timely market update and introduced the foundation of their partnership—a powerful integration designed to help financial institutions modernize payment operations without compromising on agility, scalability, or user experience.

This article summarizes their insights on leveraging centralized payment hubs, optimizing rail selection, and implementing technologies that improve performance across the RTP® network, the FedNow® Service, ACH, and wires.

Quick Links

Before diving into the agenda, the speakers introduced the organizations they represent. Paul Steinbrecher explained that Alacriti is a fintech company focused on delivering digital-first payment solutions for financial institutions. “We provide a payment platform that’s built from the ground up, cloud-native, and API-driven. We support all of the major payment rails—ACH, wires, real-time payments, card-based payments,” said Steinbrecher.

Jeff Bucher followed with an overview of Alkami, describing it as a digital banking platform that powers the front-end experience for banks and credit unions. “We really focus on enabling a modern user experience that integrates deeply with a financial institution’s back-end systems to support services like account opening, money movement, and data analytics,” said Bucher

How Alacriti and Alkami Work Together

As the demand for faster payments continues to rise, financial institutions are rethinking how they manage and route money across multiple rails. With adoption accelerating and use cases expanding, financial institutions face both the opportunity and the challenge of coordinating payments across legacy rails like ACH and Fedwire and newer, real-time options like the RTP network and the FedNow Service.

That’s where the collaboration between Alacriti and Alkami is important. Alacriti offers a modern, modular platform built for multirail orchestration. “We saw a prominent need for a payments hub, the ability to really centralize your data and also accommodate some of the new demands, like the instant payments rails out in the market,” said Steinbrecher.

The company’s solution now supports over 45 million payments annually—totaling $82 billion—across 1,500 financial institutions. Its platform architecture includes a unified money movement layer and a powerful orchestration engine that connects to all major payment rails, including RTP, FedNow, ACH, Fedwire, and Visa Direct.

Alkami, a leading provider of digital banking solutions, complements this back-end orchestration with a front-end experience that helps institutions grow and adapt quickly. “Alkami Technology is a leading cloud-based digital banking solutions provider for financial institutions,” said Bucher. “We really help our clients to grow confidently, adapt quickly, and build thriving digital communities.”

With 19.5 million live users and 266 digital banking clients as of Q1 2024, Alkami’s clients outperform peers across key metrics like deposit growth, loan growth, and return on assets. The company boasts 300+ API integrations, 16 live core integrations, and a growing SDK ecosystem that enables institutions to customize the experience while maintaining speed and scalability.

Together, the two companies are offering a seamlessly integrated solution that spans front-end digital banking and back-end payment orchestration. It’s a partnership designed to help financial institutions meet rising expectations for speed, reliability, and efficiency—while future-proofing for the next generation of payments.

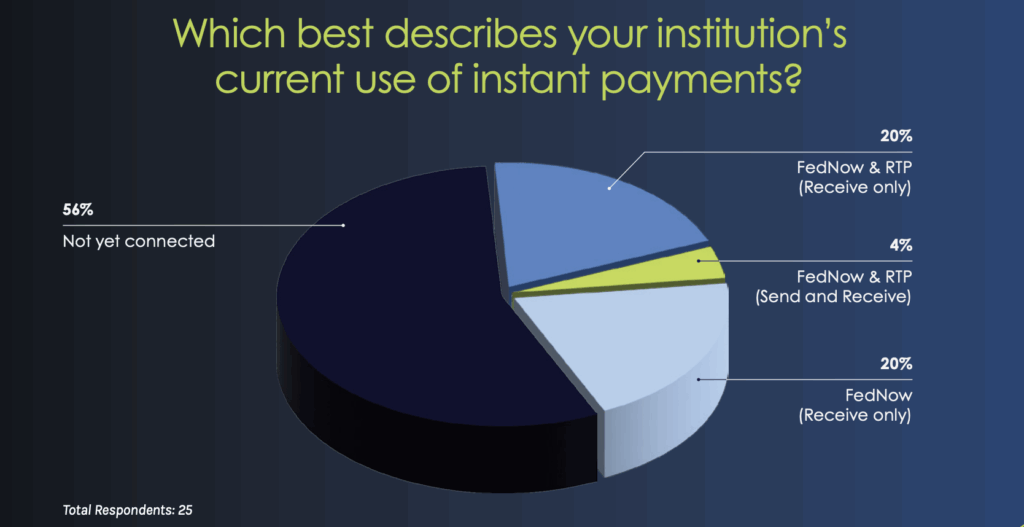

Audience Poll Question: How Institutions Are Using Instant Payments

As more businesses and consumers begin to expect real-time capabilities, those who delay may risk falling behind. However, the first audience poll revealed a surprising insight: the majority of participants indicated their institution is not yet connected to an instant payment network. This revealed an instant payments adoption gap but also an opportunity. While the majority of those polled (56%) indicated they don’t have an instant payment network, statistics show that offering free instant payments nearly doubles the likelihood that consumers will remain clients.

The presenters saw the result as a reflection of the audience’s intent. “You’re trying to learn a little bit more about why should I do this? Like, what’s the reason?” said Steinbrecher. “Seeing most of you are not connected, some of you may be connected to just one rail and then others connected to multiple rails, I find that generally on track with our overall client base.”

Multi-Rail Optimization

Financial institutions are discovering that success in the evolving payments space isn’t about choosing one network over another— it’s about orchestrating multiple rails in a way that delivers speed, reliability, and operational efficiency. Multi-rail optimization is becoming essential for financial institutions looking to meet new customer expectations and unlock growth.

Both the RTP network and the FedNow Service are experiencing rapid adoption, and the opportunity lies in leveraging both. “I would really encourage connecting to both RTP and the FedNow networks,” said Bucher. “You don’t want to, as a financial institution, miss out on somebody sending you funds…they don’t cross over.”

That lack of interoperability between the rails is a major driver behind the push toward centralized orchestration. As Steinbrecher explained, most institutions today are already moving toward support for both networks—starting with Receive capabilities and building toward full Send and Receive functionality. “The vast majority of our clients are deployed on both rails from a Receive perspective,” he said.

A key advantage of multi-rail optimization is the ability to match the right transaction to the right rail based on speed, cost, and risk tolerance. Through Alacriti’s cloud-native Orbipay Payments Hub and Alkami’s integrated digital banking platform, financial institutions can intelligently route payments across RTP, FedNow, ACH, Fedwire, and even Visa Direct. The result is a seamless front-end user experience with back-end orchestration that adapts in real time.

And customers are responding—especially outside of business hours. “We’re seeing almost 70% of all of our transactions happening after business hours,” said Steinbrecher, referencing Alacriti’s internal data. Whether it’s digital wallet withdrawals, emergency cash loans, or daily payroll payouts, real-time payments are becoming the norm for use cases where timing is critical.

Behind the scenes, that speed is made possible by deep integrations across platforms. Payments initiated through Alkami’s front end— such as A2A transfers or loan payments—are routed through Orbipay’s orchestration engine. The system supports real-time fraud checks, core banking integration, and posting—all in seconds. “We can go ahead and send an instant transfer for them. It’s basically an instant experience,” Bucher shared.

Ultimately, multi-rail optimization is about more than enabling faster payments. It’s about creating a centralized, future-ready architecture that supports customer needs, drives operational efficiency, and opens new monetization opportunities through fee-based models or differentiated user experiences. With scalable, modular platforms from Alacriti and Alkami, financial institutions of all sizes are equipped to compete—and lead—in an era of real-time money movement.

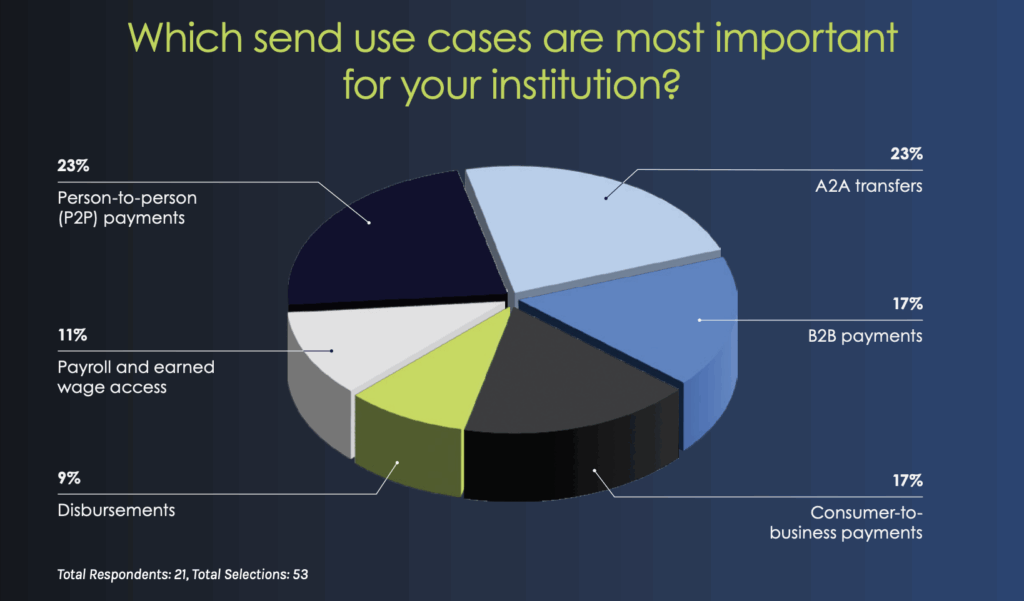

Audience Poll: What Financial Institutions Are Prioritizing for Send Use Cases

The second audience poll revealed key insights into what financial institutions see as their most important Send use cases—offering a snapshot of how the market is evolving in response to user expectations and operational needs. P2P payments and A2A payments tied with the most selections at 23% each.

These results didn’t come as a surprise. “We’ve seen a lot of our clients jump into A2A as an initial use case for Send,” said Steinbrecher. He also noted that capabilities like loan disbursements and ACH origination from a back-office portal are in active demand—indicating that institutions are looking for flexibility not just on the user-facing side but also in operations.

Bucher offered a broader context. “A2A and P2P really stand out,” he said, confirming what he’s observed in the field. However, he pointed out that consumer-to-business payments, while prevalent, face slower adoption of instant rails like RTP and FedNow. “Businesses don’t change their processes because if they find that something is working, it’s just not a priority,” he noted. But that, he believes, is temporary: “Once the businesses really start engaging there, that’s where we’re going to see the volumes really take off because that’s where the volumes are.”

While account transfers and consumer-facing use cases are currently leading the way, backend readiness and business acceptance of real-time options are expected to follow. As fintechs and financial institutions continue to enhance both the experience and the infrastructure behind these transactions, new use cases will likely rise in importance—reshaping what Send means in modern banking.

The Invisible Upgrade: How Smart Routing Is Reshaping the Payment Experience

In digital banking, the best user experiences are often the ones you never notice. That’s also true of smart routing, which determines the fastest, most cost-effective way to move money while giving users a sense of simplicity and control. Intelligent routing is transforming not just how payments are processed but how users experience those payments from start to finish—removing the friction of decision making.

This means users are shown what matters most to them: speed and cost—not the technicalities of payment rails like RTP or FedNow. Instead of jargon, they’re given clean options like “instant” or “standard,” with corresponding delivery times and fees, if any.

“The users really don’t care what payment rail it’s going over,” noted Bucher. “What they care about is who they want to pay… and how fast it gets there.” For younger users raised on digital immediacy, a threeday payment delay often feels like a system failure. The new standard is now.

But it’s not just about presenting fast and slow. Orbipay’s smart routing also includes reactionary rules to adapt in real time. For example, if a user selects an “instant” option and their financial institution lacks liquidity on the RTP network, the system can automatically reroute the payment through FedNow—without user intervention. “We can keep the payment moving rather than queuing it for anybody’s review and then halting the client’s overall experience,” said Steinbrecher.

Financial institutions can customize this behavior based on strategic priorities. Some may always prioritize the highest-speed rail, while others may prefer the lowest-cost option. These routing preferences, combined with failover logic, ensure payments are not only fast and secure but also resilient against disruptions like rail outages or cutoff times for services like wire transfers.

Behind the scenes, the collaboration between Alacriti and Alkami powers this seamless experience. A user initiates a transfer through Alkami’s digital banking platform; Alacriti’s Orbipay checks network eligibility and settlement readiness; the transaction is routed accordingly—and all the user sees is that the money is on its way.

Operational Efficiency Through Instant Payments

For financial institutions, real-time payments are often framed in terms of speed and customer expectations—but they may be just as transformative behind the scenes. The operational efficiencies provided by instant payment rails include simplified workflows, reduced overhead, and streamlined risk management.

Unlike ACH and wires, which require multiple steps, batch processes, and end-of-day reconciliations, instant payment networks function in a more direct and automated way. “The clients that have moved on to RTP and FedNow, especially when it’s just Receive, have found that it’s very, very easy to manage,” said Bucher. “They don’t need a lot of additional headcount. They don’t need a lot of extra time.”

This simplicity is largely due to the one-directional, ISO 20022-based messaging structure of the networks. These real-time systems process and settle payments individually and continuously, eliminating operational delays caused by cutoffs or weekend backlogs. Institutions don’t need to staff teams around the clock; rather, they need a partner and platform capable of automating key actions like settlement account monitoring, liquidity tracking, and exception handling

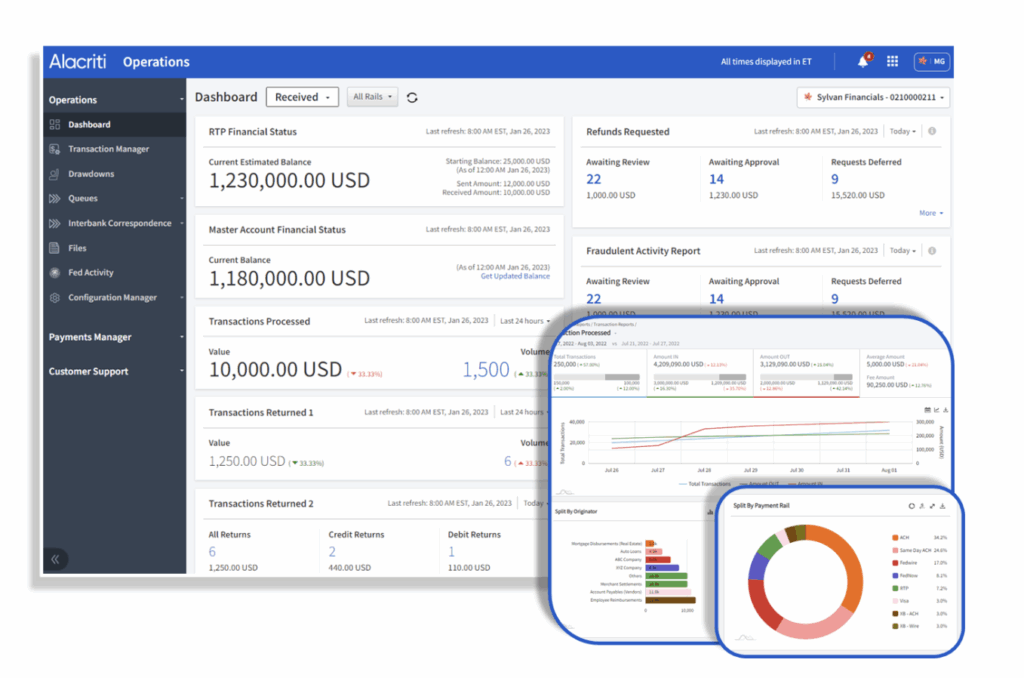

The automation made possible by Alacriti’s Orbipay Payments Hub platform further minimizes manual effort. Every instant payment instruction passes through a unified orchestration layer where custom business rules and fraud checks are executed in under a second. These checks can validate account standing, good funds availability, identity, and risk scores—automatically approving, rejecting, or queuing a transaction based on institutional tolerances.

Orbipay also provides intelligent failover routing. For example, if a payment is initiated over RTP but there’s insufficient liquidity, the platform can automatically redirect it to FedNow, ensuring uninterrupted service. These dynamic decisions are made without disrupting the end-user or requiring staff intervention.

After a payment is successfully settled, real-time status updates are sent back to the front-end platform—e.g., Alkami—providing the user with immediate confirmation. Meanwhile, financial institutions gain visibility into the entire transaction lifecycle through Orbipay’s robust back-office portal. This portal allows staff to search, review, manage exceptions, initiate payments on behalf of clients, and export detailed reports for internal analysis or compliance.

From API connectivity to dashboard customization and reporting, Orbipay is designed to integrate seamlessly across departments— enabling institutions to modernize without burdening operations. “We see instant payments as the priority rail for that reason. There’s just less operational impact, especially on the receive side,” Steinbrecher noted.

Ultimately, the promise of real-time payments isn’t just about meeting customer demand for immediacy—it’s about transforming how institutions work, freeing up resources, and enabling smarter, leaner payment operations.

To learn more about how proactive digital outreach can improve

payment performance, reduce costs, and strengthen customer

loyalty, watch the full webinar, Shifting the Payments Paradigm: Why

Digital Outreach Matters to Your Bottom Line.

Alacriti’s Loan Payments, is a customizable electronic billing and payments

solution for businesses and financial institutions of all sizes. Orbipay EBPP

offers convenient and flexible choices that include all the payment channels,

payment methods, and payment options expected from a modern digital bill

pay experience.