Wire & Global Transfers Made Simple

Moving money around the world shouldn’t be a headache. Orbipay Payments Hub plugs seamlessly into your existing systems to deliver fast, reliable global transfers with competitive FX rates and total transparency.

Challenges

A Growing Need for Change

Moving money internationally requires more than just speed—it requires predictable outcomes and clear visibility. Disconnected payment systems create inefficiencies and make it difficult to support modern global channels. Common pain points include:

Legacy infrastructure that lacks the agility to scale or support emerging cross-border options like stablecoins

Manual workflows and siloed processing that increase costs and slow down international delivery

Disjointed user experiences that leave customers in the dark, forcing them to call support for status updates

Complex compliance burdens, like Regulation E and Dodd-Frank, that strain staff and increase operational risk

The potential annual cost for large banks for global operational costs due to delays, fees, and penalties

in correspondent banking relationships over the last decade

The average time for a single payment investigation

is the projected global spending on financial crime compliance in 2024

Solutions

Fast, Transparent, and Revenue-Ready Global Transfers

With Orbipay Payments Hub for Cross-Border, you can unify international wires, Visa Direct, and ACH on a single platform to deliver the speed and transparency your customers expect—all while maximizing your FX revenue potential.

Value

Why Orbipay Payments Hub for Cross-Border?

Engineered for global reach, operational control, and financial growth

Our centralized hub integrates directly with your existing core and digital banking to modernize international money movement. It provides a unified gateway to global networks, allowing your institution to:

- Unify disparate payment rails

- Provide real-time status updates and end-to-end traceability

- Intelligently identify the most effective processor for every currency and corridor

Key Capabilities

Deliver Fast, Transparent Global Transfers

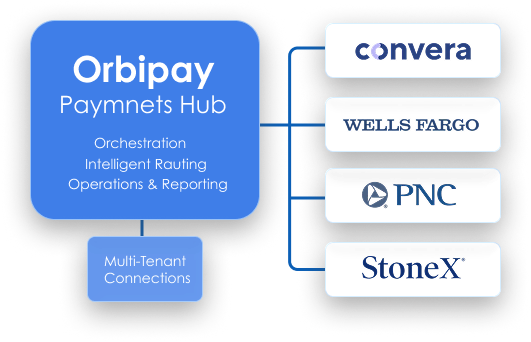

Orbipay Payments Hub for Cross-Border provides a unified, ISO 20022-native platform designed to modernize international money movement. It bridges the gap between legacy systems and modern rails—like international wires and Visa Direct—by centralizing orchestration, intelligent routing, and real-time visibility. Integrate seamlessly with your existing core and digital banking systems to provide:

International Wires:

Live today through our partnerships with Convera, supporting 200+ countries and 140+ currencies.

Intelligent Path Selection:

Optimize transactions by speed or cost using a rules-based engine that automatically routes payments to the best processor for each currency and corridor.

Real-Time Status & Traceability:

Eliminate inquiry calls with on-demand status updates and full transaction transparency for both staff and customers.

Processing Bank Integrations:

Expanding connectivity with providers, including Wells Fargo, PNC, and StoneX, giving flexibility to work with your preferred partner.

Automated Compliance:

Built-in support for Regulation E and Dodd-Frank disclosures, and automated documentation to reduce operational risk.

ISO 20022 Data Model:

Native ISO 20022 messaging ensures global interoperability and carries richer data for faster straight-through processing.

Explore Other Payment Rails Supported by the Payments Hub

The Alacriti Payments Hub connects financial institutions to multiple payment rails through a single platform.

Key Benefits

The Business Case for Modernizing Global Transfers With Alacriti

Optimized FX Revenue & Margin Management

Full Traceability & Transparency

Unified Payment Processing & Settlement

Future-Proof Your Payments Infrastructure

Turnkey Compliance

Increased Accountholder Satisfaction

Customer Perspectives

We Help Customers Achieve Superior Business Outcomes

Desert Financial Credit Union Partners With Alacriti to Unify Instant and Legacy Payments

The unified approach positions Desert Financial to expand domestic and cross-border payment capabilities while improving operational efficiency and member experience.

Frequently Asked Questions

How do global transfers through Orbipay Payments Hub work?

Orbipay Payments Hub acts as an aggregator, connecting your institution to a vast network of global correspondent banks and regional low-value networks. It uses a “bring your own provider” model, integrating with partners like Convera, StoneX, and Wells Fargo to handle back-end processing, while Alacriti manages the front-end origination, reporting, and compliance. The system automatically presents users with transparent options based on their urgency, ranging from low-fee global ACH to instant transfers or standard international wires.

Are cross-border payments through a hub secure and compliant?

Yes. Modern hubs enhance security by utilizing ISO 20022-standardized messaging, which carries richer data to improve fraud screening and global interoperability. Our solution further secures transactions by automating mandatory regulatory disclosures and documentation, ensuring your institution meets strict consumer protection standards for every global transfer.

How does "intelligent routing" actually lower costs?

Instead of sending every international payment through the same expensive wire path, the hub’s engine analyzes the currency and destination in real time. It then automatically selects the most cost-effective or fastest route—such as a low-fee global ACH for non-urgent transfers or an instant push-to-card via Visa Direct for speed.

Does this solution support emerging options like stablecoins?

Yes. The platform is built to be future-proof. Because it uses a unified orchestration layer, you can easily add support for emerging payment methods—including stablecoins—as they become more mainstream, ensuring your institution stays ahead of fintech competitors.

Related Resources

Modernize Your Payments. Maximize Your Efficiency.

See how Alacriti helps insurers reduce costs, increase on-time collections, and improve the policyholder’s experience.

Sources:

For some large banks, global operational costs tied to delays, fees, and penalties can reach “as high as $20 million per year.”

A key driver of modernization is the decline in traditional banking networks: correspondent banking relationships have fallen by over 50% in the last decade, making it harder for banks to provide low-cost cross-border services without modern technology. (Source: Celent, cited by American Banker)

Banks report that payment investigations typically take 5–8 days, driving poor customer experience and operational drag.

Global spending on financial crime compliance operations (a major source of exceptions and investigations) was projected to be $155.3 billion in 2024.