The short answer is no. But the reality is more nuanced and more urgent.

Small and mid-sized businesses (SMBs) are increasingly using fintechs for payments, invoicing, and cash flow management. At first glance, that trend suggests fintechs are winning the relationship. But the data tells a different story. SMBs aren’t choosing fintechs over their financial institutions. They’re turning to fintechs because they have to.

According to a Datos Insights survey in Q1 2026, while 71% of SMBs use at least one fintech provider, 85% say they would prefer to access those same capabilities through their primary financial institution. That gap—between usage and preference—is where the real opportunity lies.

Why SMBs Turned to Fintechs

SMBs didn’t go looking for more providers. They went looking for better outcomes. As payments have become more central to day-to-day operations, SMBs have needed faster ways to move money, clearer visibility into their cash position, and less manual work to manage receivables and payables. Fintechs responded quickly with targeted solutions that addressed these needs directly.

Meanwhile, many financial institutions focused on improving digital access rather than rethinking how SMBs actually operate. The result was incremental improvement, but not transformation. SMBs could log in more easily, but many core operational challenges remained—such as reconciling payments, tracking incoming funds, and understanding real-time cash flow.

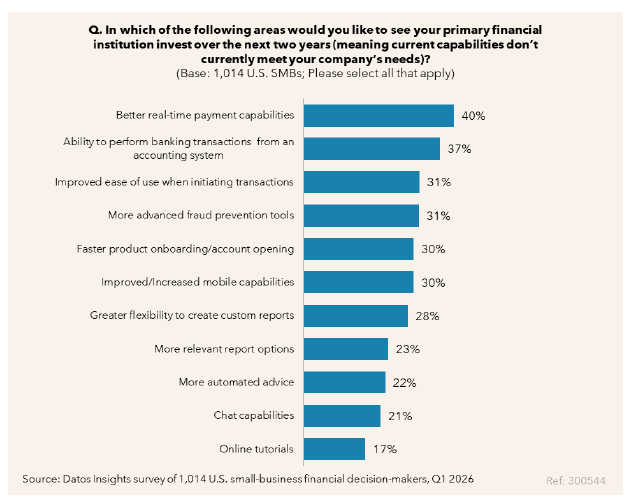

Datos research shows that SMBs consistently rank real-time payments, payment visibility, and reconciliation support among their top priorities. Fintechs gained traction because they solved specific problems faster.

The Fragmentation Problem SMBs Now Face

What started as a workaround has created a new challenge. Today, many SMBs operate across multiple platforms—one for payments, another for invoicing, another for expense tracking, and yet another for cash flow monitoring. Businesses frequently rely on multiple tools to manage core financial functions, creating a fragmented operating environment.

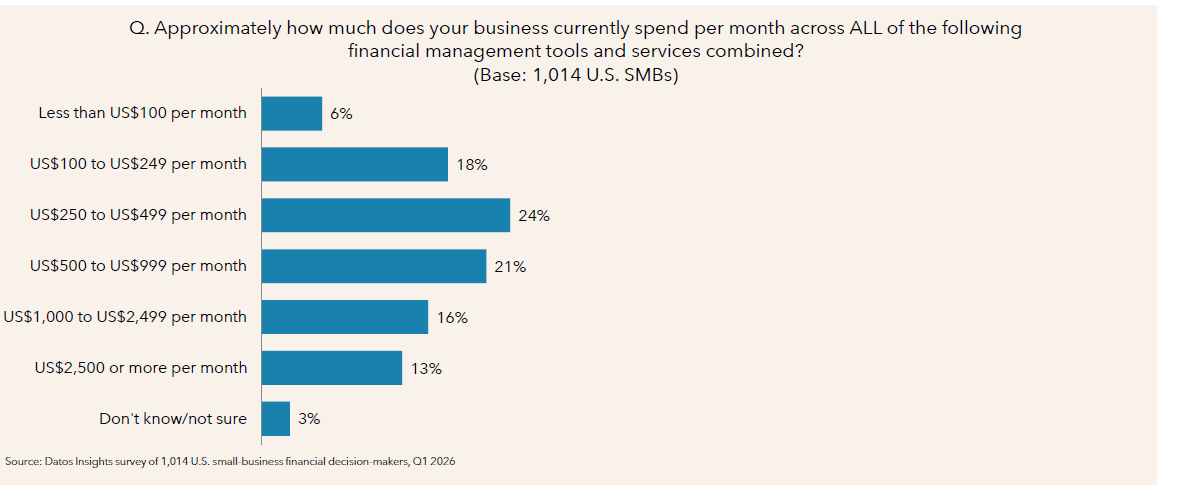

Over time, this fragmentation introduces friction. Data is spread across systems. Reconciliation becomes more manual. Costs increase as subscription tools stack up. And perhaps most importantly, visibility into the business becomes less clear, not more.

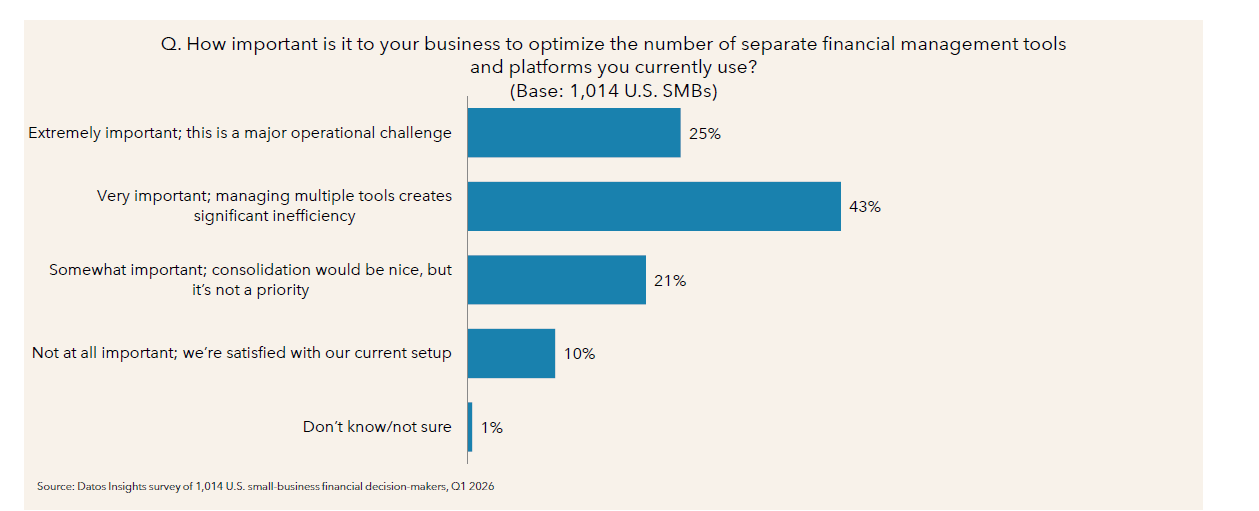

Unsurprisingly, SMBs are starting to push back. A majority now say that consolidating financial tools is important, with many describing it as a significant operational challenge.

What SMBs Want Now

The assumption has long been that SMBs are highly price-sensitive. But the data suggests they are more so value-sensitive.

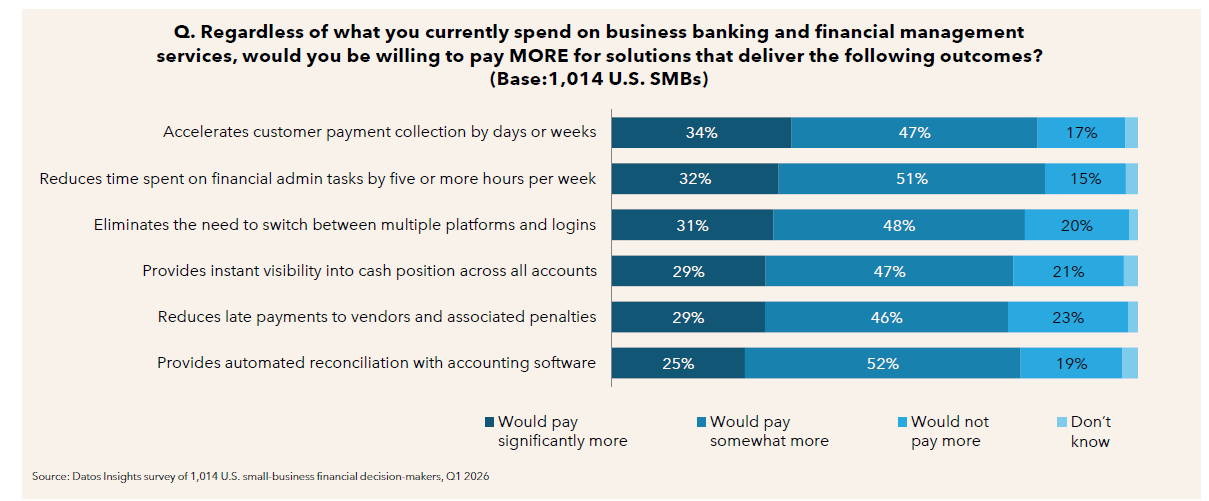

SMBs are willing to pay for solutions that deliver measurable impact—saving time, accelerating payments, and reducing operational complexity. In fact, a large majority indicate they would pay more for capabilities like faster payment collection, automated reconciliation, and real-time visibility into their cash position.

They want the functionality they found in fintech tools—speed, automation, flexibility—but delivered in a more unified experience. SMBs want real-time visibility into cash flow, payments that move without delay, and reconciliation and reporting processes that require minimal manual effort. All these capabilities should be embedded into the systems they already trust.

Are Financial Institutions Losing SMBs?

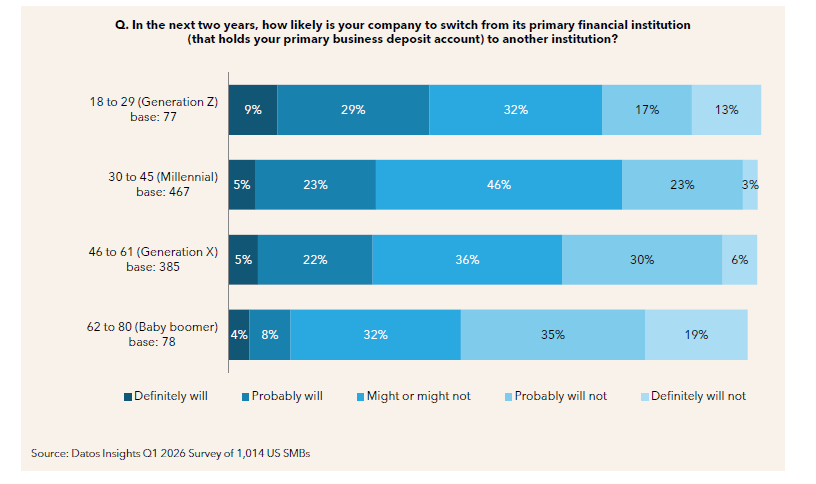

Not entirely—but the margin for error is shrinking. SMBs remain optimistic about their growth, and that optimism is changing how they evaluate their banking relationships. Confident businesses are more willing to explore alternatives if better options exist.

At the same time, the reasons SMBs would consider switching financial institutions are becoming more explicit. Payment capabilities—automation, real-time processing, and flexibility—are now among the top drivers of change.

Rather than trust or tenure, banking relationships are increasingly defined by utility.

So, Do SMBs Prefer Fintechs?

No. They prefer outcomes. Fintechs have become essential because they solve problems better—at least for now. Financial institutions still hold the most important advantage: the primary relationship. SMBs still rely on banks and credit unions for deposits, lending, and core financial services. What’s changed is where they go to get work done.

In effect, SMBs are asking their financial institutions to evolve from service providers into platforms that support how their business actually runs. The institutions that can deliver that experience won’t just compete with fintechs—they’ll become the preferred place for SMBs to run their business.

To learn how credit unions can create a more unified experience for SMB members, visit Alacriti’s credit union solutions page. See how a modern approach can help simplify operations and strengthen relationships.

Alacriti’s centralized payment platform, Orbipay Payments Hub, provides innovation opportunities and the ability to make smart routing decisions at the financial institution to meet their individual needs. Financial institutions can take full ownership of their payments and control their evolution with TCH’s RTP® network, the FedNow® Service, Zelle®, Fedwire, ACH, and Visa Direct, all on one cloud-based platform. Alacriti’s Orbipay Loan Payments is a customizable electronic billing and payments solution for businesses and financial institutions of all sizes. Orbipay Loan Payments offers convenient and flexible choices that include all the payment channels, payment methods, and payment options expected from a modern digital bill pay experience. To speak with an Alacriti payments expert, please contact us at (908) 791-2916 or info@alacriti.com.