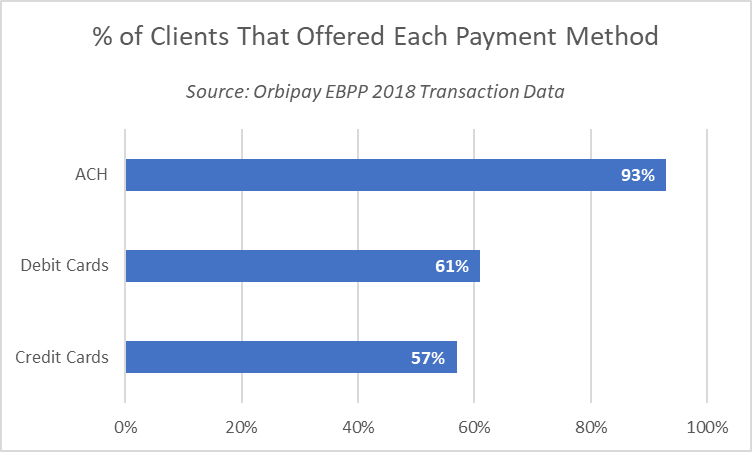

Payment card information changes more often than you might think. Individual cards are frequently lost or stolen, expiration dates come due regularly, and mass reissuance can be prompted by card upgrades and/or security breaches.

More and more customers save their payment methods electronically to take advantage of automatic payment options. While this provides the benefit of “setting it and forgetting it”, it also means that updating saved card information might not be top-of-mind when that data changes. Billers that rely on direct intervention from customers to update stale funding sources can be left chasing late bill payments and missing out on timely revenue.

A credit card updater solution helps minimize the hassle of missed bill payments due to outdated card information. Billers that subscribe to this service receive fresh card data seamlessly, preserving incoming cash flow and reducing the burden on internal resources tasked with recovering missed bill payments.

Credit card updater, part of our Orbipay EBPP (Electronic Bill Presentment and Payment) solution, automatically submits expiring cards to merchant processors to automatically obtain new payment card information. Here are five benefits of credit card updater for bill payments.

- Maintain accurate customer card account information.

Bill payments are only as good as their funding sources. Credit card updater refreshes saved payment card information automatically, meaning your organization always has the most up-to-date data.

- Reduce interrupted bill payments.

Credit card updater’s automated process helps reduce the number of interrupted bill payments, supporting continuous incoming revenue that your organization relies on.

- Deliver a better customer experience.

Credit card updater eliminates the need for customers or members to manually update their card information when it changes. It also helps them avoid late or missed payments, creating a more positive experience throughout their customer journey.

- Prevent service disruptions.

Late or missed payments due to outdated card information can have serious consequences for bill payers. Credit card updater can help reduce service disruptions and prevent account delinquencies by supplying the most accurate card data to your organization.

- Improve operational efficiency.

When a bill payment fails, contacting customers or members to update their funding source information can be a significant burden for your internal teams. Credit card updater automates this process, giving your staff more time to focus on other organizational initiatives.

The Bottom Line: Credit card updater automates the burdensome process of refreshing stale saved payment card information. The solution is often offered as part of an overall EBPP, usually alongside automated card expiration notifications and card expiration reporting, meaning that adopting credit card updater can be as simple as talking to your EBPP provider.

Updated from a blog post originally published September 25, 2019.

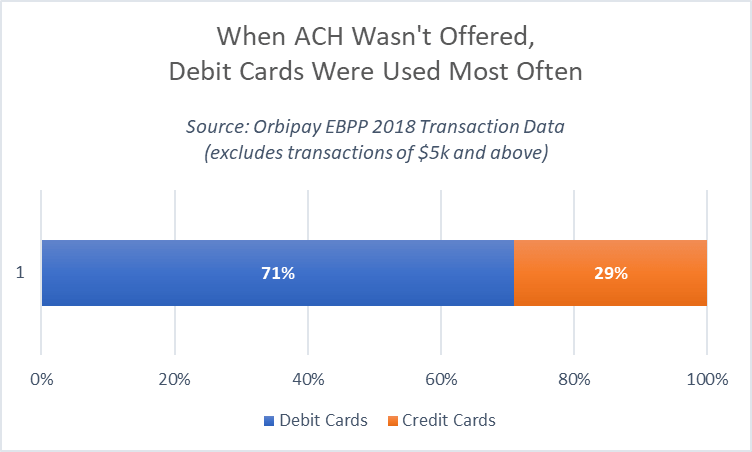

Nacha rules require originators of WEB debit entries to use a “commercially reasonable fraudulent transaction detection system”, making it necessary for a real-time bank account validation process. Read more in Nacha Rule Extensions.

Alacriti’s Orbipay EBPP is a customizable electronic billing and payments solution for businesses and financial institutions of all sizes. Credit Card Updater is just one of several Orbipay EBPP features available to help you accelerate receivables. For more information, please contact us at info@alacriti.com.